$100,000 Term Life Insurance Policy Rates

$100,000 Whole Life Insurance Policy Rates

| Age | Female | Male |

|---|---|---|

| 20 | $57 | $64 |

| 25 | $66 | $75 |

| 30 | $78 | $89 |

| 35 | $92 | $106 |

| 40 | $110 | $126 |

| 45 | $134 | $155 |

| 50 | $168 | $192 |

| 55 | $219 | $245 |

| 60 | $283 | $318 |

| 65 | $365 | $413 |

| 70 | $506 | $566 |

| 75 | $705 | $794 |

| 80 | $942 | $1,041 |

| 85 | $1,176 | $1,321 |

| Monthly rates are calculated at a preferred non-tobacco rating, rounded to the nearest dollar, and are valid as of 03/09/2026. | ||

$100,000 Universal Life Insurance Policy Rates

| Age | Female | Male |

|---|---|---|

| 20 | $33 | $37 |

| 25 | $33 | $37 |

| 30 | $36 | $42 |

| 35 | $45 | $53 |

| 40 | $54 | $63 |

| 45 | $64 | $77 |

| 50 | $73 | $90 |

| 55 | $83 | $102 |

| 60 | $107 | $135 |

| 65 | $131 | $167 |

| 70 | $202 | $286 |

| 75 | $278 | $408 |

| 80 | $405 | $601 |

| 85 | $617 | $881 |

| Monthly rates are calculated at a non-tobacco preferred rating, rounded to the nearest dollar, and are valid as of 03/09/2026. | ||

How Does Each Type Of Life Insurance Work?

All types of life insurance will ultimately pay your loved ones a tax-free cash payment of $100,000 (or however much coverage you buy). There’s never any tax due on a life insurance payout, nor are there restrictions on how the money is spent.

That said, there are various types of policies that all work differently.

- Whole life insurance: A whole life policy is a type of permanent coverage that lasts for the insured’s entire life. Regardless of age, the policy will remain in force indefinitely if you reliably make all your payments. Also, the policy premiums cannot increase, and the coverage cannot decrease. There’s also a cash value component that accrues over time. You can withdraw the cash value and spend it any way you want.

- Term life insurance: A term life policy is temporary coverage. The policy will last for a set period, such as 10, 20, or 30 years.

- Universal life insurance: Universal life is a complex form of permanent coverage that offers flexibility in premium payments and cash value access.

It’s critically important to select the coverage type that best fits your goals and budget.

Factors That Influence The Cost

It’s helpful to remember that every life insurance company has different underwriting and pricing. That said, insurers use specific variables to determine how much life insurance costs for each applicant.

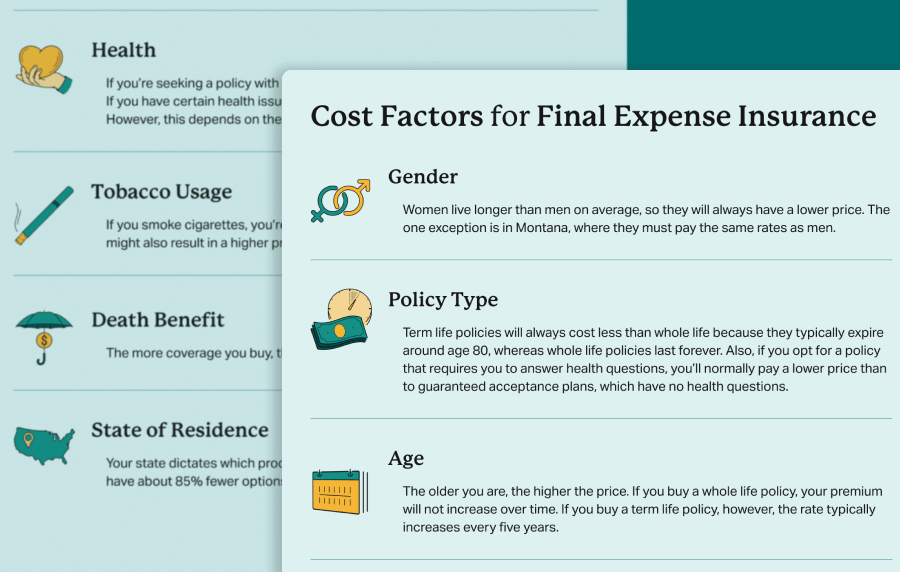

- Type of policy: The type of coverage you select will have a major impact on the cost of a life insurance policy. Term life is the cheapest, followed by universal life, then whole life.

- Gender: Females always pay about 30% less for life insurance products because they live longer than men. So, if you’re male, expect to pay higher rates than females. The one exception to this rule is for the state of Montana. They have a law prohibiting life insurers from pricing males and females differently. Sadly, life insurance companies in Montana simply charge women whatever they charge men. In effect, Montana state law raised prices for women.

- Age: The older you are, the higher your rates will be. That’s why buying funeral life insurance or any other type is always a good idea when you’re younger. For example, one of the main reasons people buy children’s life insurance is to lock in super-low rates.

- Health: In short, specific health issues that are high risk might increase the cost (not always), but many do not. For example, minor issues such as high blood pressure or cholesterol are relatively benign. Insurers rarely charge higher premiums for those types of conditions. However, if you have diabetes, COPD, or kidney disease, you’ll likely pay a higher rate because those are higher-risk conditions. Also, every life insurance company will accept and reject different health conditions. One of the keys to finding the best rate is to identify which company is most accepting of all your health conditions. You should work with a broker who can compare multiple insurance companies on your behalf. That way, they can determine which insurer is most friendly to your health conditions.

- Tobacco usage: On average, people who consume tobacco products (cigarettes, chew, cigars, snuff) don’t live as long as those who don’t. For that reason, expect higher premiums (about 40%-60% higher) if you’re a tobacco user. Also, if you stop using tobacco, you’ll have to wait until it has been at least 12 months before you’re eligible for non-tobacco pricing.

- Coverage amount: The more coverage you buy, the higher your premium will be. Also, prices for life insurance are proportional. For example, a $25,000 whole life policy is 1/4th the cost of a $100,000 whole life policy. A $75,000 whole life policy is 75% of the cost of $100K. A $50,000 whole life plan is ½ the cost, and $10,000 would be 1/10th the price of $100K.

Application Underwriting Options

There are three underwriting options for a $100,000 life insurance policy. The method you choose will determine how long it takes for your application to be approved. It also influences the cost.

No-exam

A no medical exam policy is often called “simplified issue” or “non-med.” As the name implies, you don’t have to meet with a nurse to give a blood and urine sample. The application only requires that you answer questions about your health history.

The insurance company will also electronically review your driving record and medication history. These types of applications generally render an approval or decline within 15 minutes to a few business days.

Fully underwritten

Unlike simplified policies, a fully underwritten application requires you to complete a medical exam.

You’ll meet with a nurse who will collect a blood and urine sample. They will also measure your height, weight, and blood pressure. Additionally, the insurer will order copies of all your medical records (from all physicians you’ve seen).

Once they have all this data, they will determine if you’re approved and the final price. On average, fully underwritten applications will take six to eight weeks to be approved or declined.

Yes, fully underwritten applications can take a long time to complete, but the wait can be worth it because it usually results in a lower price.

No health questions (guaranteed issue whole life)

A guaranteed issue life insurance policy does not require you to answer health questions or take an exam. Simply put, they guarantee your approval.

While guaranteed approval may sound wonderful, there are drawbacks to consider.

Primarily, the waiting period is the biggest downfall to be aware of. Life policies with no health questions all have a two-year waiting period.

If you die during the waiting period, the insurer will only refund your premiums plus a small amount of interest.

Aside from the waiting period, the other downside of these policies is cost.

Since the insurer knows nothing about your health, it carries a high amount of risk. Due to the higher risk, the insurance is significantly more expensive.

Lastly, guaranteed issue policies are always a type of whole life insurance and typically have a maximum coverage amount of $25,000.

If you want $100,000 in total guaranteed acceptance coverage, you would have to buy four $25K guaranteed issue plans from four different insurance companies.

- Nationally licensed life insurance agent with over 16 years of experience.

- Personal annual production that puts him in the top .001% out of all life insurance agents in the nation.

Anthony Martin is a nationally licensed insurance expert with over 16 years of experience and has personally served over 10,000 clients with their life insurance needs. He frequently authors entrepreneurial and life insurance content for Forbes, Inc.com, Newsweek, Kiplinger, and Entreprenuer.com. Anthony has been consulted as an expert life insurance source for dozens of high-profile websites such as Forbes, Bankrate, Reuters, Fox Business, CNBC, Investopedia, Insurance.com, Yahoo Finance, and many more.

- Nationally licensed life insurance agent with over 20 years of experience

- Best selling Amazon author.

Jeff Root is a nationally licensed life insurance expert with over 20 years of experience. He has personally helped over 3000 clients with their life insurance needs. Jeff is a best-selling Amazon author and the managing partner of a highly successful insurance brokerage that manages over 2,500 licensed insurance agents across the USA. He has been a featured life insurance source for prestigious websites such as Forbes, Bloomberg, MarketWatch, Nerdwallet, and many more.

- Nationally licensed life insurance agent with over 15 years of experience

- Best selling Amazon author of five insurance sales books.

David Duford is a nationally licensed insurance expert with over 15 years of experience. He has personally helped more than 15,000 clients buy life insurance. David has been featured as an expert source for highly authoritative publications such as A.M. Best and Insurancenewsnet. He also runs one of the largest Youtube channels to help aspiring insurance agents serve their clients better.

- Nationally licensed life insurance agent with over 20 years of experience

- Best selling Amazon author.

Jeff Root is a nationally licensed life insurance expert with over 20 years of experience. He has personally helped over 3000 clients with their life insurance needs. Jeff is a best-selling Amazon author and the managing partner of a highly successful insurance brokerage that manages over 2,500 licensed insurance agents across the USA. He has been a featured life insurance source for prestigious websites such as Forbes, Bloomberg, MarketWatch, Nerdwallet, and many more.

- Nationally licensed life insurance agent with over 15 years of experience

- Best selling Amazon author of five insurance sales books.

David Duford is a nationally licensed insurance expert with over 15 years of experience. He has personally helped more than 15,000 clients buy life insurance. David has been featured as an expert source for highly authoritative publications such as A.M. Best and Insurancenewsnet. He also runs one of the largest Youtube channels to help aspiring insurance agents serve their clients better.

Choice Mutual often cites third-party websites to provide context and verification for specific claims made in our work. We only link to authoritative websites that provide accurate information. You can learn more about our editorial standards, which guide our mission of delivering factual and impartial content.

-

live longer. https://www.cdc.gov/nchs/products/databriefs/db328.htm

-

a law prohibiting. https://www.upi.com/Archives/1985/10/01/Unisex-insurance-law-begins/7442496987200/

-

don't live as long. https://archive.cdc.gov/#/details?q=https://www.cdc.gov/tobacco/data_statistics/fact_sheets/health_effects/tobacco_related_mortality/index.htm&start=0&rows=10&url=https://www.cdc.gov/tobacco/data_statistics/fact_sheets/health_effects/tobacco_related_mortality/index.htm