How Does A 30-Year Term Life Policy Work?

A 30-year term life insurance policy lasts for 30 years, at which point it will end. Should you die during that time, the insurer will pay the death benefit as cash (tax-free) to the beneficiaries you chose. They can spend the money with no restrictions.

It’s most common for 30-year policies to have a fixed premium for the entire term. However, some insurers may have regular price increases every 5 or 10 years.

Normally, insurance companies sell 30-year term policies only to people who are 55 or younger.

What Will Happen After 30 Years?

When the 30 years are up, the coverage ends, and you are no longer insured. Plus, the insurance company keeps the premiums you paid over the last three decades (unless you had a return of premium riderReturn of Premium Rider

A rider that will refund all premiums paid at the end of the policy term. It's uncommon for insurers to offer these riders, and they will significantly increase the policy's cost.).

What Options Are There Before 30 Years Are Over?

Assuming you want to continue having life insurance coverage, you generally have the following options before a term life insurance policy ages out.

- Renew it at a higher price point: Many insurers will offer you the option to renew the policy before the first term ends. The nice part about this option is that there is no qualification process. If you agree to the renewal, they will reissue the policy at a greatly increased price.

- Convert to whole life: Nearly every single term life insurance policy automatically includes a conversion privilege clause. It gives you the right to convert from term life to whole life without having to endure any sort of underwriting. Keep in mind that if you convert, there will be a rather large price increase. If you compare whole life to term life, the biggest difference is the cost. Whole life insurance always costs substantially more than term life. In addition, when you convert, they calculate your rate based on your current age, and since you’re older, that also contributes to the higher cost.

- Buy a new policy: If you let the policy expire, your only option is to buy a new one. That’s generally feasible unless you’re really up in age. At most, 90 is the absolute oldest someone can be and still be able to buy a new life insurance policy.

How Much Does A 30 Year Term Life Policy Cost?

Below are sample 30-year term life insurance quotes for various ages and coverage amounts. Keep in mind that many variables determine the cost of life insurance, so you may find that your price varies from these examples. Also, shorter-term options, such as 20-year or 10-year terms, will cost less.

When Is It A Good Idea To Opt For A 30-Year Term Policy?

A 30-year term life policy is ideal for people in the following circumstances:

- Have dependent spouse and children– If your family relies on your income, you need life insurance to replace your income. A 30-year term will provide a large amount of coverage at a low cost for a period of time until your children are well into adulthood.

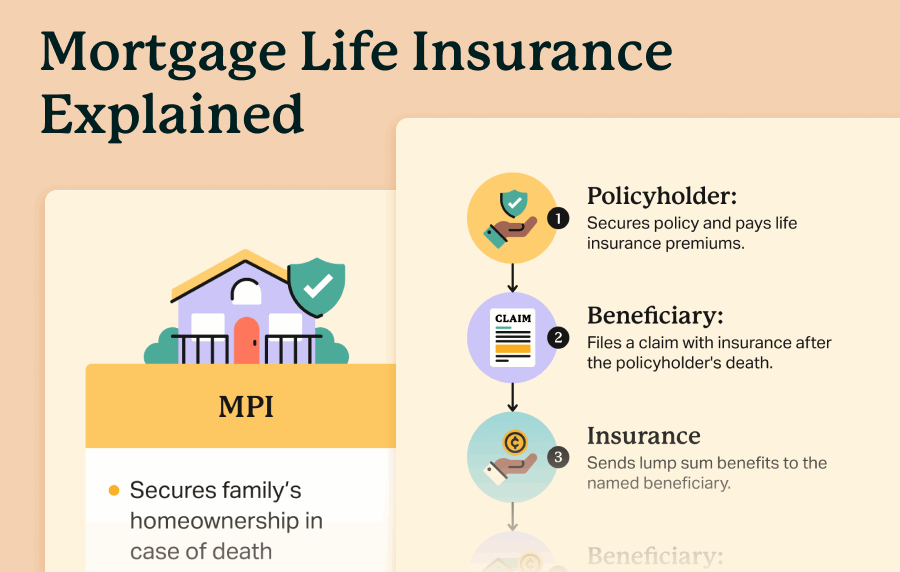

- Want to pay off your mortgage– At most, a mortgage lasts 30 years, so a 30-year term will easily ensure that it will pay off your mortgage (assuming you have a sufficient death benefit to cover the balance). Interestingly, companies that market “mortgage protection insurance” are typically selling a 30-year term life policy.

- Other long-term financial debts– If you have other financial debts that you would like to pay off, a 30-year term will last for more than enough time.

When is a 30-year term not a good idea?

It’s unwise to rely on a term policy (be it 30 years or any other length) to cover a permanent need. For example, if you want life insurance to cover your final expenses, term insurance is not recommended.

That’s because term life insurance generally expires around age 80. If you outlive the policy (which most do), then you won’t have coverage to pay off your final expenses. Instead, you want to opt for a final expense life insurance policy, which lasts forever, so you can rest easy knowing it will always be there when you need it.

How Do You Qualify And Buy A 30-Year Term Policy?

Some 30-year term life policies require a medical exam, and some don’t. It varies by insurer. Here’s a breakdown of both options:

- No medical exam: You don’t have to meet with a nurse to provide a blood and urine sample. Instead, you simply answer some health and lifestyle questions. In addition, the insurance company will electronically access various databases that give it information about your current and prior health history. In general, no exam applications are approved within a few business days.

- With a medical exam: Life insurance that requires a medical exam is called “fully underwritten”. You complete the medical exam and answer extensive questions about your health and lifestyle. Additionally, the insurer will request your formal medical records from all your current and prior doctors (from the last 10 years). After they gather all of this data, they can determine if you’re approved and what the final price will be. The entire process typically takes 4-6 weeks before the application is approved. The main advantage of fully underwritten products is their lower cost.

To actually buy the policy, some insurers (not many) offer online applications. With those, you submit all your information online, sign electronically, and never need to speak with an agent.

Conversely, most insurers (over 90%) require you to buy their policies from a licensed agent who is authorized to sell their products. You’d meet with the agent either virtually or in person. They will gather all your information and read you the required disclosures and health and lifestyle questions. Then it’s just a matter of waiting for the insurer to approve your application.

Regardless of how you buy, every company will mail you a physical policy (some will also email it) directly to your home address.

Frequently Asked Questions

If you’re approved for a term life policy, there will be no waiting period. There are no term life policies that have a two-year waiting period.

“Cashing out” a life insurance policy is only applicable to whole life and universal life policies, as they have cash value, whereas term life policies do not. That said, a term life policy can indeed be cancelled. An insurer can refuse your request to end the policy. When you cancel a term life policy, there is no cash surrender value, unlike with a whole life or universal life policy.

You cannot borrow money from a 30-year term (or any term for that matter) because term life insurance does not accrue cash value.

A 40-year term is the longest any company offers. They aren’t common, and you will need to be 40-45 years old or younger to be eligible.

No insurer offers guaranteed acceptance term life insurance. To qualify for a 30-year term (or shorter), you must, at a minimum, answer health questions.

- Nationally licensed life insurance agent with over 16 years of experience.

- Personal annual production that puts him in the top .001% out of all life insurance agents in the nation.

Anthony Martin is a nationally licensed insurance expert with over 16 years of experience and has personally served over 10,000 clients with their life insurance needs. He frequently authors entrepreneurial and life insurance content for Forbes, Inc.com, Newsweek, Kiplinger, and Entreprenuer.com. Anthony has been consulted as an expert life insurance source for dozens of high-profile websites such as Forbes, Bankrate, Reuters, Fox Business, CNBC, Investopedia, Insurance.com, Yahoo Finance, and many more.

- Nationally licensed life insurance agent with over 20 years of experience

- Best selling Amazon author.

Jeff Root is a nationally licensed life insurance expert with over 20 years of experience. He has personally helped over 3000 clients with their life insurance needs. Jeff is a best-selling Amazon author and the managing partner of a highly successful insurance brokerage that manages over 2,500 licensed insurance agents across the USA. He has been a featured life insurance source for prestigious websites such as Forbes, Bloomberg, MarketWatch, Nerdwallet, and many more.

- Nationally licensed life insurance agent with over 15 years of experience

- Best selling Amazon author of five insurance sales books.

David Duford is a nationally licensed insurance expert with over 15 years of experience. He has personally helped more than 1,500 clients buy life insurance. David has been featured as an expert source for highly authoritative publications such as A.M. Best and Insurancenewsnet. He also runs one of the largest YouTube channels to help aspiring insurance agents serve their clients better.

- Nationally licensed life insurance agent with over 20 years of experience

- Best selling Amazon author.

Jeff Root is a nationally licensed life insurance expert with over 20 years of experience. He has personally helped over 3000 clients with their life insurance needs. Jeff is a best-selling Amazon author and the managing partner of a highly successful insurance brokerage that manages over 2,500 licensed insurance agents across the USA. He has been a featured life insurance source for prestigious websites such as Forbes, Bloomberg, MarketWatch, Nerdwallet, and many more.

- Nationally licensed life insurance agent with over 15 years of experience

- Best selling Amazon author of five insurance sales books.

David Duford is a nationally licensed insurance expert with over 15 years of experience. He has personally helped more than 1,500 clients buy life insurance. David has been featured as an expert source for highly authoritative publications such as A.M. Best and Insurancenewsnet. He also runs one of the largest YouTube channels to help aspiring insurance agents serve their clients better.