How Does Decreasing Term Life Insurance Work?

Decreasing term insurance, like all term life policies, provides coverage for a specific period of time- typically 10, 15, 20, 25, or 30 years. Regardless of which term length you choose, the policy will define how much the death benefit reduces at the specified intervals. The death benefit reduction may occur annually, semiannually, or every 5 years.

When you die, the insurance company will pay out the death benefit to your beneficiaries. The amount paid out will be consistent with whatever the death benefit is at your time of death. For example, if your initial death benefit was $100,000 and it eventually decreased to $75,000 at the time of your death, the insurer would only pay out $75,000.

When you reach the end of the term, the coverage terminates, and you’re simply uninsured.

Most decreasing term life policies have a fixed premium for the entire term. However, some may have a rate reduction whenever the death benefit declines.

The advantage of decreasing term life insurance compared to level term is that it’s less expensive. If you know your life insurance needs will decrease over time, this type of term policy can be advantageous, as it will save you money.

Main Reasons Someone Should Opt For Decreasing Term

A decreasing term life policy can be an excellent and least expensive option for anyone in the following circumstances.

Small business owners

Many have business loans or credit card debt. A decreasing term can be the most cost-effective way to ensure these liabilities are paid off should the business owner die.

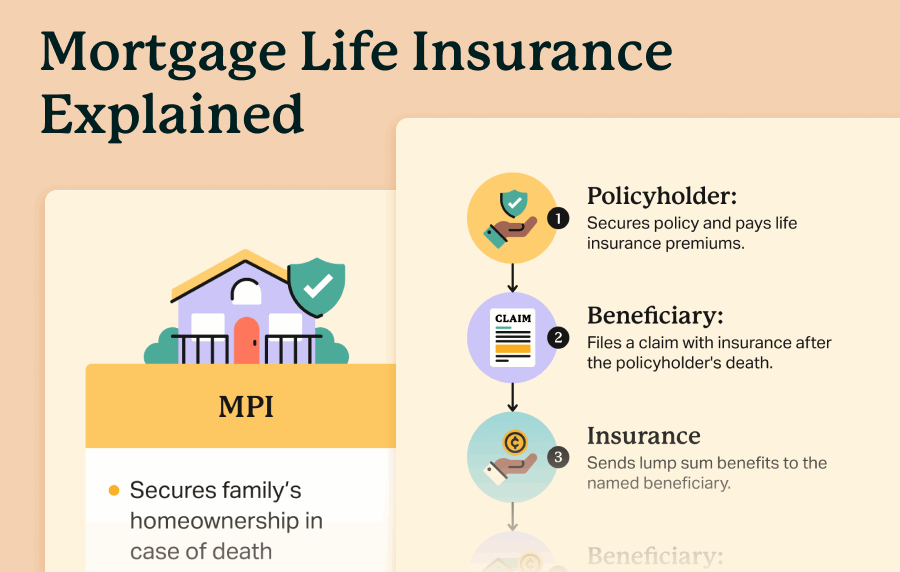

Mortgage coverage

Many Americans buy life insurance as mortgage protection coverage. They want to ensure that the mortgage is paid off upon death.

A decreasing term is ideal in this scenario because it decreases as the mortgage balance does. You’d save money compared to buying a level term policy.

Other financial debts

If you have car notes, personal loans, or credit card debts, this type of policy is perfect.

Children who will become adults within 5-10 years

It’s wise to have life insurance to replace your income so your dependents can continue their lifestyle in the event of your death.

If your minor dependents will become adults soon, a decreasing term is a suitable option that will save you money compared to a level term, since your needs will decrease once the children become self-sustaining adults.

What Are The Advantages And Disadvantages Of Decreasing Term?

- Lower cost: Decreasing term life insurance is generally the least expensive type of term life coverage.

- Perfect for debt coverage: If you’re buying life insurance to ensure a debt is paid off, a decreasing term policy is ideal, since it decreases as the debt does. You don’t need to pay more for a level term policy with a fixed death benefit.

- Term insurance is very affordable: Term life insurance is unquestionably the least expensive type of life insurance.

- Minimal availability: Very few life insurance companies offer decreasing term life policies. So if you’re in the market for one, you have less ability to compare multiple providers to find the best deal.

- Not good for unexpected life changes: As life so often does, your life insurance needs may change, where you need a policy that doesn’t have a decreasing death benefit. A decreasing term life insurance policy cannot be converted into one with a fixed benefit. You’re stuck with it. If your circumstances change and you need coverage that doesn’t decrease, your only recourse is to buy an entirely new policy.

- Expiration: Because it’s a term insurance policy, it will expire, leaving you uninsured at some point.

Decreasing Term Life Vs Other Types Of Term Life Insurance

Depending on your needs, a decreasing term may or may not be the optimal type of policy. Here’s how it compares to other types of term life insurance:

- Level: Level term life insurance has a locked-in premium and death benefit.

- Convertible: Convertible term life insurance is a policy that gives you the right to convert to permanent whole life insurance. The conversion privilege is guaranteed, and there is no medical qualification.

- Renewable: Renewable term life insurance allows you to renew your policy at the end of the initial term. The renewed policy will cost more than what you were initially paying. Also, you won’t need to answer health questions or take a medical exam.

- Increasing: Increasing term life insurance has a death benefit that grows over time. Oftentimes, the premium increases as the death benefit does, but with some insurers, it remains fixed.

Frequently Asked Questions

Every insurer is different regarding how much the death benefit reduces and the intervals at which the reductions occur. When you buy the policy, there will be a schedule that shows conclusively when the reductions will happen and what the values will be.

Decreasing term policies cannot be converted to level term policies, which have a fixed death benefit. If you have a decreasing term policy, the only way to transition to a fixed benefit policy would be to buy a new one with the same or a different provider.

When a decreasing term policy reaches its end, it terminates. You will no longer be insured and the insurance company will keep the premiums you’ve paid.

- Nationally licensed life insurance agent with over 16 years of experience.

- Personal annual production that puts him in the top .001% out of all life insurance agents in the nation.

Anthony Martin is a nationally licensed insurance expert with over 16 years of experience and has personally served over 10,000 clients with their life insurance needs. He frequently authors entrepreneurial and life insurance content for Forbes, Inc.com, Newsweek, Kiplinger, and Entreprenuer.com. Anthony has been consulted as an expert life insurance source for dozens of high-profile websites such as Forbes, Bankrate, Reuters, Fox Business, CNBC, Investopedia, Insurance.com, Yahoo Finance, and many more.

- Nationally licensed life insurance agent with over 20 years of experience

- Best selling Amazon author.

Jeff Root is a nationally licensed life insurance expert with over 20 years of experience. He has personally helped over 3000 clients with their life insurance needs. Jeff is a best-selling Amazon author and the managing partner of a highly successful insurance brokerage that manages over 2,500 licensed insurance agents across the USA. He has been a featured life insurance source for prestigious websites such as Forbes, Bloomberg, MarketWatch, Nerdwallet, and many more.

- Nationally licensed life insurance agent with over 15 years of experience

- Best selling Amazon author of five insurance sales books.

David Duford is a nationally licensed insurance expert with over 15 years of experience. He has personally helped more than 15,000 clients buy life insurance. David has been featured as an expert source for highly authoritative publications such as A.M. Best and Insurancenewsnet. He also runs one of the largest Youtube channels to help aspiring insurance agents serve their clients better.

- Nationally licensed life insurance agent with over 20 years of experience

- Best selling Amazon author.

Jeff Root is a nationally licensed life insurance expert with over 20 years of experience. He has personally helped over 3000 clients with their life insurance needs. Jeff is a best-selling Amazon author and the managing partner of a highly successful insurance brokerage that manages over 2,500 licensed insurance agents across the USA. He has been a featured life insurance source for prestigious websites such as Forbes, Bloomberg, MarketWatch, Nerdwallet, and many more.

- Nationally licensed life insurance agent with over 15 years of experience

- Best selling Amazon author of five insurance sales books.

David Duford is a nationally licensed insurance expert with over 15 years of experience. He has personally helped more than 15,000 clients buy life insurance. David has been featured as an expert source for highly authoritative publications such as A.M. Best and Insurancenewsnet. He also runs one of the largest Youtube channels to help aspiring insurance agents serve their clients better.