Average Cost Of Term Life Insurance

Below are term life insurance rates for coverage amounts ranging from $100,000 to $1,000,000.

10-year term rates

The life insurance rates below are for a 10-year term life policy.

20-year term rates

The life insurance rates below are for a 20-year term life policy.

30-year term rates

The life insurance rates below are for a 30-year term life policy.

Average Cost Of Whole Life Insurance

Below are whole life insurance rates by age for coverage amounts ranging from $50,000 to $100,000.

Average Cost Of Final Expense Insurance

Below are final expense life insurance rates by age for coverage amounts ranging from $5,000 to $50,000.

Average Cost Of Guaranteed Acceptance Life Insurance

Below are guaranteed acceptance life insurance rates by age for coverage amounts ranging from $10,000 to $25,000.

Average Cost Of Universal Life Insurance

Below are universal life insurance rates by age for coverage amounts ranging from $50,000 to $500,000.

Average Cost Of Children’s Life Insurance

Below are children’s life insurance rates by age for coverage amounts ranging from $10,000 to $50,000.

| Age | $10,000 | $25,000 | $50,000 |

|---|---|---|---|

| 0-4 | $4.61 | $10.02 | $19.04 |

| 5-9 | $5.43 | $12.08 | $23.17 |

| 10-14 | $6.15 | $13.87 | $26.75 |

| 15-17 | $7.75 | $17.87 | $34.75 |

| Source for monthly prices: Choice Mutual child quote calculator. Rates are unisex and valid as of 03/09/2026. | |||

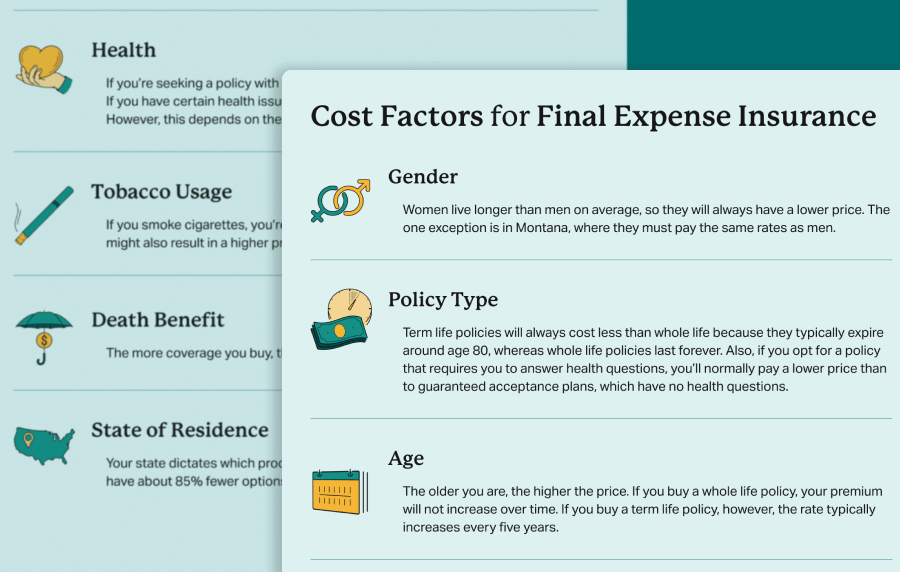

Factors That Determine The Cost Of Life Insurance

At a high level, the cost of a life insurance policy is based on life expectancy. Many factors go into this, and depending on the type of policy and the company, some or all of the following factors may apply, such as:

- Gender: Men will always (except in Montana) pay roughly 30% more for life insurance products because, on average, they don’t live as long as women. The CDC’s current statistics show that men typically live to age 75.8, compared with 81.1 for women.

- Age: Unsurprisingly, life insurance costs more when you’re older. Younger people are less likely to die, which is why rates are lower when you’re younger.

- Type of policy: Whether you’re seeking term life insurance, whole life insurance, or a universal life policy will have a major impact on your life insurance rates. Term is always the cheapest type of policy, followed by universal life; whole life is always the most expensive.

- Length of the term (applies to term life policies only): With term life insurance, you choose how long the policy will last, which affects the price. The typical term lengths are 10, 15, 20, 25, and 30 years. The longer the term, the higher the cost.

- Amount of coverage: The more coverage you buy, the higher the cost.

- Type of underwriting: Underwriting is the method by which the insurer determines if you’re eligible for any given policy. There are three types: fully underwritten, simplified issue, and guaranteed issue. Fully underwrittenFully Underwritten

A type of life insurance underwriting that requires the applicant to undergo a medical exam. In addition, the insurer will formally request copies of all your medical records from every physician you've seen in the last decade. Once all of this data is compiled, the insurer will determine whether you're approved and, if so, which rate classification you're eligible for. These rate classifications typically include: Preferred-Plus, Preferred, Standard, and various Sub-Standard ratings. The better the rating, the lower your premiums will be. is the cheapest option because the insurer requires you to complete a medical exam, answer health questions, and they subpoena all your medical records. Simplified issueSimplified Issue

Simplified issue underwriting is essentially the same as accelerated underwriting except for A) there are fewer health questions to answer, B) approvals are faster, and C) they often accept more risky applicants. The insurer still gathers health and lifestyle information about you via various databases. That information, along with your answers to the health questions, is fed into an algorithm that determines if you're approved. options will cost more because, while you still have to answer health questions, you don’t need to take a medical exam. Finally, guaranteed acceptanceGuaranteed Acceptance

There are no health questions or a medical exam. The insurer literally knows nothing about your health, and therefore, you cannot be denied for any prior medical issues. policies do not require you to answer health questions or take a medical exam, making it the most expensive type since the insurance company is insuring your life while knowing absolutely nothing about your health. - Health history: Having pre-existing conditions can affect your premiums, but not always. It all depends on: A) the ailments you’ve had, B) their severity, C) the timing of your issues, and D) how well you’ve followed your physician’s treatment program. For example, a heart attack 10 years ago won’t be a considerable hindrance to eligibility, let alone the cost. However, a heart attack one year ago would.

- Lifestyle: If you engage in high-risk hobbies such as mountain climbing or boat racing, expect higher life insurance premiums. Similarly, certain high-risk occupations, such as crane operation, can drive up prices.

- Nicotine or tobacco habits: First, if you use cigarettes, life insurance will cost you much more (sometimes 100% more) since they dramatically reduce life expectancy. For other forms of tobacco, such as snuff or vaping, you should expect higher prices from most companies and products. However, some insurers will offer non-tobacco prices for non-cigarette forms of nicotine.

- Driving record: If you have too many points on your record or serious offenses (DUI or reckless driving), insurers will probably charge you a higher rate.

- Criminal history: If you have any convictions for misdemeanors or felonies, it can impact your premiums or even disqualify you. It depends on the nature of the crime and the time of the sentence. The same is true if you’re on parole.

- Financial history: Credit scores don’t affect life insurance rates, but a bankruptcy can. Recent bankruptcies will prompt insurers to charge higher premiums for certain types of life insurance.

- Family health history: Insurers often ask whether your immediate family members have ever had diabetes, heart disease, or other conditions. If so, it could affect your rate.

- Alcohol habits: Moderate alcohol usage is not going to affect your premium. However, if you’ve ever had a history of abuse, that will have a significant impact on your eligibility and cost. If you consume a large amount of alcohol (less than the threshold of being an alcoholic), it will very likely lead to higher rates.

- Optional policy riders: Insurers often allow you to enhance your coverage by adding optional riders, such as an accidental death riderAccidental Death Rider

The insurer will pay out double the death benefit if the insured dies from an accident.. These riders cost extra (varies by rider) and thus affect the net premium you pay for your life insurance policy. - State of residence: Life insurance companies don’t have unique rates for each state. However, the state you live in dictates which products are available to you. Also, if you live in Montana, there is a law requiring insurers to charge women the same rate as they charge men. The result of that law is that women in Montana pay about 30% more than women in all other states.

- How you pay your premiums: Insurers often impose a surcharge for those who pay monthly or quarterly by direct bill (you mail payments) or by credit card. However, if you pay monthly via automatic bank account deduction (using the routing and account numbers), semi-annually (every six months), or annually, there will be no additional cost.

How Much Life Insurance Do You Need?

As a guiding principle to determine how much life insurance you need, ask yourself the following question: “If I were to die today, what would the life insurance payout money be used for?” The answer to that question will identify all your needs, and from that point, you can assign a monetary value to them.

Some common needs include: paying off funeral expenses, replacing income, or paying off a mortgage.

Another, more guided approach is to use the DIME formula, which stands for Debt, Income, Mortgage, and Education. You add up all those variables to calculate the total amount of life insurance you need. You can also use a life insurance calculator, which will walk you through the process.

Tips For Finding The Most Affordable Life Insurance Rates

There are many practical actions you can take to get a lower life insurance premium and secure the most affordable life insurance possible.

- Take a medical exam: A medical exam gives the insurer detailed up-to-date information about your health. This reduces their risk, resulting in a lower cost.

- Opt for autopayments from your bank: Most insurers offer their lowest price to people who set up automatic payments from their bank account using the routing and account numbers.

- Pay in bulk either semi-annually or annually: Insurance companies often grant some sort of discount for paying in bulk. Depending on the cost of your life insurance policy, you could save hundreds of dollars annually by paying in bulk. Keep in mind that paying quarterly will generally not result in a discount.

- Shop around: Every insurance company charges a different rate (especially if you have any pre-existing conditions). You’ll very likely obtain a lower life insurance cost by comparing 5-10 insurers before making any final decisions.

- Utilize the services of an independent agent: Independent agents represent multiple providers rather than just one. Conversely, a captive agent can represent only one company. An independent agent can be invaluable because they can compare offers from many providers to find you the best deal. Just be sure to select an agent who has access to at least ten providers.

- Be open to insurance companies that aren’t household names: In 2021, there were 737 life insurance companies in the USA. While it’s likely less now, the total number is still quite high. Perhaps 5% of life insurance companies are household names, such as State Farm or Mutual of Omaha. Ultimately, you should be open to companies that you’ve not heard of so that you’re not limiting yourself to a tiny fraction of the overall market. Insurers that you’re not familiar with aren’t untrustworthy or financially unstable. They simply have a business model that does not involve mass marketing to become nationally renowned.

- Don’t wait: Your health (let alone life) is not promised tomorrow. If you want life insurance coverage, you’ll get the lowest rate by buying it as soon as possible. Waiting to purchase a life insurance policy can only make it more expensive.

- Quit smoking: People who smoke cigarettes will pay 50-100% more for life insurance because they have a 300% higher chance of dying prematurely. If you smoke now and quit for at least one year, you’ll qualify for substantially lower premiums.

- Improve your health: Many pre-existing health issues can and will raise the cost of life insurance. Improving your health, such as losing weight, lowering your blood pressure, improving your cholesterol, reducing your A1C, and more, can all result in lower premiums.

- Buy term life insurance: Without question, term life insurance is the least expensive type of life insurance.

Frequently Asked Questions

When getting a life insurance quote, insurers ask for your state of residence because where you live dictates which products are available to you. For example, a given product may be available in Texas but not in California.

Women pay less for life insurance because they typically live longer than men.

While $9.95 is a low price for life insurance, it depends on what you’re getting in return. Often, life insurance companies will advertise very low teaser rates to entice customers to contact them. In reality, the low price they quoted (e.g., the $9.95 plan from Colonial Penn) provides minimal coverage.

Generally speaking, life insurance will cost more if you don’t take a medical exam. However, no medical exam life insurance options have gotten less expensive and are now very close to the cost of policies that require a medical exam.

Whole life insurance policies will always cost more than term life policies.

How an insurer reacts to marijuana use varies by company. Some may charge you a tobacco-user’s rate (which would be higher), and some won’t. It all depends on the product you’re applying for and the insurer. They all have their own rules.

- Nationally licensed life insurance agent with over 16 years of experience.

- Personal annual production that puts him in the top .001% out of all life insurance agents in the nation.

Anthony Martin is a nationally licensed insurance expert with over 16 years of experience and has personally served over 10,000 clients with their life insurance needs. He frequently authors entrepreneurial and life insurance content for Forbes, Inc.com, Newsweek, Kiplinger, and Entreprenuer.com. Anthony has been consulted as an expert life insurance source for dozens of high-profile websites such as Forbes, Bankrate, Reuters, Fox Business, CNBC, Investopedia, Insurance.com, Yahoo Finance, and many more.

- Nationally licensed life insurance agent with over 20 years of experience

- Best selling Amazon author.

Jeff Root is a nationally licensed life insurance expert with over 20 years of experience. He has personally helped over 3000 clients with their life insurance needs. Jeff is a best-selling Amazon author and the managing partner of a highly successful insurance brokerage that manages over 2,500 licensed insurance agents across the USA. He has been a featured life insurance source for prestigious websites such as Forbes, Bloomberg, MarketWatch, Nerdwallet, and many more.

- Nationally licensed life insurance agent with over 15 years of experience

- Best selling Amazon author of five insurance sales books.

David Duford is a nationally licensed insurance expert with over 15 years of experience. He has personally helped more than 15,000 clients buy life insurance. David has been featured as an expert source for highly authoritative publications such as A.M. Best and Insurancenewsnet. He also runs one of the largest Youtube channels to help aspiring insurance agents serve their clients better.

- Nationally licensed life insurance agent with over 20 years of experience

- Best selling Amazon author.

Jeff Root is a nationally licensed life insurance expert with over 20 years of experience. He has personally helped over 3000 clients with their life insurance needs. Jeff is a best-selling Amazon author and the managing partner of a highly successful insurance brokerage that manages over 2,500 licensed insurance agents across the USA. He has been a featured life insurance source for prestigious websites such as Forbes, Bloomberg, MarketWatch, Nerdwallet, and many more.

- Nationally licensed life insurance agent with over 15 years of experience

- Best selling Amazon author of five insurance sales books.

David Duford is a nationally licensed insurance expert with over 15 years of experience. He has personally helped more than 15,000 clients buy life insurance. David has been featured as an expert source for highly authoritative publications such as A.M. Best and Insurancenewsnet. He also runs one of the largest Youtube channels to help aspiring insurance agents serve their clients better.

Choice Mutual often cites third-party websites to provide context and verification for specific claims made in our work. We only link to authoritative websites that provide accurate information. You can learn more about our editorial standards, which guide our mission of delivering factual and impartial content.

-

life expectancy. https://mort.soa.org/

-

CDC’s current statistics. https://www.cdc.gov/nchs/fastats/life-expectancy.htm

-

they dramatically reduce life expectancy. https://www.medicalnewstoday.com/releases/9703#1

-

a law. https://www.upi.com/Archives/1985/10/01/Unisex-insurance-law-begins/7442496987200/

-

DIME formula. https://www.johnhancock.com/ideas-insights/how-much-life-insurance-do-you-need.html

-

life insurance calculator. https://lifehappens.org/life-insurance-needs-calculator/

-

737 life insurance companies. https://www.acli.com/-/media/acli/public/files/factbook/11fb22chapter11industryrankings.pdf

-

300% higher chance. https://newsroom.heart.org/news/smokers-especially-those-who-begin-young-are-three-times-more-likely-to-die-prematurely