$25,000 Whole Life Insurance Policy Rates

| Age | Female | Male |

|---|---|---|

| 40 | $45 | $54 |

| 45 | $52 | $63 |

| 50 | $55 | $71 |

| 55 | $64 | $84 |

| 60 | $76 | $103 |

| 65 | $97 | $130 |

| 70 | $127 | $169 |

| 75 | $172 | $238 |

| 80 | $241 | $335 |

| 85 | $335 | $477 |

| 86 | $423 | $585 |

| 87 | $510 | $686 |

| 88 | $596 | $788 |

| 89 | $683 | $888 |

| Source for monthly prices: Choice Mutual quote calculator. Rates are calculated at a non-tobacco rating, rounded to the nearest dollar, and are valid as of 03/09/2026. | ||

$25,000 Guaranteed Acceptance Life Insurance Policy Rates

| Age | Female | Male |

|---|---|---|

| 45 | $68 | $90 |

| 50 | $75 | $99 |

| 55 | $92 | $112 |

| 60 | $105 | $141 |

| 65 | $124 | $170 |

| 70 | $158 | $215 |

| 75 | $220 | $282 |

| 80 | $316 | $391 |

| 85 | $393 | $480 |

| Source for monthly prices: Choice Mutual quote calculator. Rates are for Mutual of Omaha's guaranteed acceptance whole life policy, rounded to the nearest dollar, and are valid as of 03/09/2026. | ||

$25,000 Term Life Insurance Policy Rates

| Age | Female | Male |

|---|---|---|

| 50 | $18 | $26 |

| 55 | $22 | $36 |

| 60 | $32 | $50 |

| 65 | $44 | $67 |

| 70 | $74 | $95 |

| Source for monthly prices: Choice Mutual quote calculator. Rates are calculated at a non-tobacco rating, rounded to the nearest dollar, and are valid as of 03/09/2026. | ||

How Does Each Type of Policy Work?

There are different types of life insurance that all work differently. The key is to choose the right kind of policy that is best suited to accomplish your goal.

If you shop for life insurance based on price alone, you will regret it. You must consider all the terms and conditions of a policy to make the right choice.

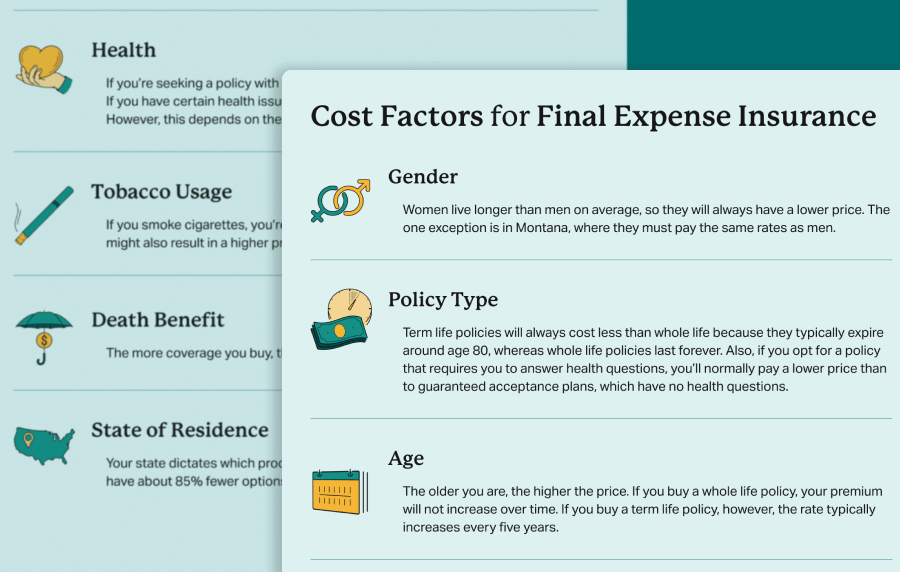

- Whole life: Whole life insurance is a type of permanent life insurance. It comes with ironclad guarantees. The premium cannot increase, the death benefit cannot decrease, and the policy lasts forever. In addition, it will build cash value.

- Term life: A term life insurance policy is a type of temporary coverage. By design, the policy will terminate after a number of years or at a specific age. Some term policies may last 10, 20, or 30 years. On the other hand, some term policies may last until you reach a certain age. For example, AARP’s final expense insurance expires at age 80. Generally speaking, all term policies will end around age 80 plus or minus a few years. Once a term policy ends, you don’t have coverage and don’t get your money back. You’re simply uninsured and need to find a new policy if you want life insurance.

- Guaranteed acceptance: Guaranteed issue life insurance policies have no health questions because your approval is guaranteed. There is always a two-year waiting period. If you die during the first two years, the insurer will only refund your premiums plus roughly 10% interest. Presently, all guaranteed issue policies are a type of whole life insurance. No insurance company offers a term life policy with guaranteed acceptance. Remember, to get life insurance with no waiting period, you must answer health questions.

Tips For Finding The Best Policy

Doing online research is excellent because it gives you an idea of what companies are available. You can also see approximate life insurance rates.

In the end, you should work with an independent broker who can compare multiple companies on your behalf to find you the best price.

Keep in mind that the least expensive life insurance policies are always sold through licensed insurance agents rather than being sold online directly by the insurance company.

To get the lowest price possible for a $25,000 whole life final expense policy, find a reputable independent agency that partners with ten more insurance companies.

Then, let them compare options from multiple providers to find which company will give you the best burial insurance policy.

Working with an independent agency is free, and the insurance won’t cost more because of their services.

Frequently Asked Questions

The cash value in any whole life policy varies based on your premium and how long the policy has been in force. For example, a 65-year-old female who buys a $25,000 whole policy should expect to have approximately $2,500 in cash value after five years and $6,000 after ten years. A 65-year-old male would have roughly $3,000 in cash value after five years and $7,000 after ten years. Every policy (regardless of which company you buy from) will include a schedule that clearly outlines the guaranteed cash value for each year the policy is in force.

No life insurance company offers a life policy with a $25,000 death benefit where you can take a medical exam to potentially lower the price. At this coverage amount, all policies are no exam. Some policies are even guaranteed acceptance, which have no medical exam and no health questions.

- Nationally licensed life insurance agent with over 16 years of experience.

- Personal annual production that puts him in the top .001% out of all life insurance agents in the nation.

Anthony Martin is a nationally licensed insurance expert with over 16 years of experience and has personally served over 10,000 clients with their life insurance needs. He frequently authors entrepreneurial and life insurance content for Forbes, Inc.com, Newsweek, Kiplinger, and Entreprenuer.com. Anthony has been consulted as an expert life insurance source for dozens of high-profile websites such as Forbes, Bankrate, Reuters, Fox Business, CNBC, Investopedia, Insurance.com, Yahoo Finance, and many more.

- Nationally licensed life insurance agent with over 20 years of experience

- Best selling Amazon author.

Jeff Root is a nationally licensed life insurance expert with over 20 years of experience. He has personally helped over 3000 clients with their life insurance needs. Jeff is a best-selling Amazon author and the managing partner of a highly successful insurance brokerage that manages over 2,500 licensed insurance agents across the USA. He has been a featured life insurance source for prestigious websites such as Forbes, Bloomberg, MarketWatch, Nerdwallet, and many more.

- Nationally licensed life insurance agent with over 15 years of experience

- Best selling Amazon author of five insurance sales books.

David Duford is a nationally licensed insurance expert with over 15 years of experience. He has personally helped more than 15,000 clients buy life insurance. David has been featured as an expert source for highly authoritative publications such as A.M. Best and Insurancenewsnet. He also runs one of the largest Youtube channels to help aspiring insurance agents serve their clients better.

- Nationally licensed life insurance agent with over 20 years of experience

- Best selling Amazon author.

Jeff Root is a nationally licensed life insurance expert with over 20 years of experience. He has personally helped over 3000 clients with their life insurance needs. Jeff is a best-selling Amazon author and the managing partner of a highly successful insurance brokerage that manages over 2,500 licensed insurance agents across the USA. He has been a featured life insurance source for prestigious websites such as Forbes, Bloomberg, MarketWatch, Nerdwallet, and many more.

- Nationally licensed life insurance agent with over 15 years of experience

- Best selling Amazon author of five insurance sales books.

David Duford is a nationally licensed insurance expert with over 15 years of experience. He has personally helped more than 15,000 clients buy life insurance. David has been featured as an expert source for highly authoritative publications such as A.M. Best and Insurancenewsnet. He also runs one of the largest Youtube channels to help aspiring insurance agents serve their clients better.