$75,000 Term Life Insurance Policy Rates

$75,000 Whole Life Insurance Policy Rates

| Age | Female | Male |

|---|---|---|

| 20 | $36 | $41 |

| 25 | $43 | $50 |

| 30 | $51 | $59 |

| 35 | $61 | $70 |

| 40 | $75 | $86 |

| 45 | $93 | $108 |

| 50 | $116 | $136 |

| 55 | $144 | $171 |

| 60 | $175 | $202 |

| 65 | $216 | $249 |

| 70 | $280 | $325 |

| 75 | $371 | $431 |

| 80 | $480 | $559 |

| Monthly rates are calculated at a non-tobacco preferred rating, rounded to the nearest dollar, and are valid as of 03/09/2026. | ||

$75,000 Universal Life Insurance Policy Rates

| Age | Female | Male |

|---|---|---|

| 20 | $32 | $38 |

| 25 | $39 | $45 |

| 30 | $44 | $49 |

| 35 | $48 | $53 |

| 40 | $60 | $65 |

| 45 | $69 | $75 |

| 50 | $82 | $90 |

| 55 | $97 | $109 |

| 60 | $124 | $144 |

| 65 | $143 | $173 |

| 70 | $216 | $252 |

| 75 | $354 | $418 |

| 80 | $515 | $677 |

| Monthly rates are calculated at a non-tobacco preferred rating, rounded to the nearest dollar, and are valid as of 03/09/2026. | ||

How Does Whole Life & Term Life Insurance Work?

Whole life insurance is a type of permanent policy that lasts for the insured’s entire life. There is an ironclad guarantee that the death benefit and premium cannot change. It will also build cash value, like a behind-the-scenes equity account. A term life policy is temporary coverage that lasts for a specified number of years and does not build cash value.

Universal life insurance is permanent coverage like whole life. It also builds cash value. What’s unique about a UL policy is that you can typically adjust your premiums and the cash value growth is generally much higher.

For all types, the insurance company will pay your beneficiaries through a tax-free check when you die. There are no restrictions on how they use that money, so they can spend it on funeral expenses, debts, medical bills, or anything else. Additionally, any remaining funds are theirs to keep.

Underwriting Options: Exam, No-Exam & No Health Questions

There are three types of underwriting (varies by the company) for a whole life insurance policy with a $75,000 death benefit.

- No-Exam: Also commonly known as “simplified issue,” a no-medical exam policy does not require you to meet with a nurse to give a blood and urine sample. Qualification is only dependent upon your answers to health questions. In addition to the health questions, the insurance company will electronically review your medication history because that provides thorough insight into your overall health history.

- Guaranteed Issue: Also commonly known as “guaranteed acceptance life insurance,” this type of policy has no underwriting whatsoever. That means you don’t have to take an exam or answer health questions. These policies frequently appear on TV, such as the Colonial Penn 9.95 plan. It’s imperative to remember that all guaranteed acceptance policies have a two-year waiting period. The insurance provider will only refund your premiums if you die in the first 24 months. Guaranteed issue plans are typically unavailable to young adults because most providers make these plans available starting at age 45-50. Also, these types of policies generally have a maximum coverage amount of $25,000. So, if you want $75,000 in coverage, you’ll need to buy multiple policies from different providers to get to $75K. For example, you might need to buy a $25K policy from AAA, Gerber Life, and Mutual of Omaha.

- Fully Underwritten: This option requires you to meet with a nurse so they can weigh you, measure your weight, check your blood pressure, and collect a blood and urine sample. In addition, the insurance company will order copies of all your medical records from all your physicians. After receiving all this information, the insurance company will determine if they can offer you coverage and at what price. Generally, fully underwritten applications take 4-8 weeks for a policy to be approved or declined. The main advantage of fully underwritten applications is the price. Because the insurance company knows everything about your health (in great detail), the insurance costs less.

There will be no waiting period if a fully underwritten or no-exam policy is approved. It’s advisable to only opt for a guaranteed issue policy if your medical conditions prevent you from qualifying for anything else.

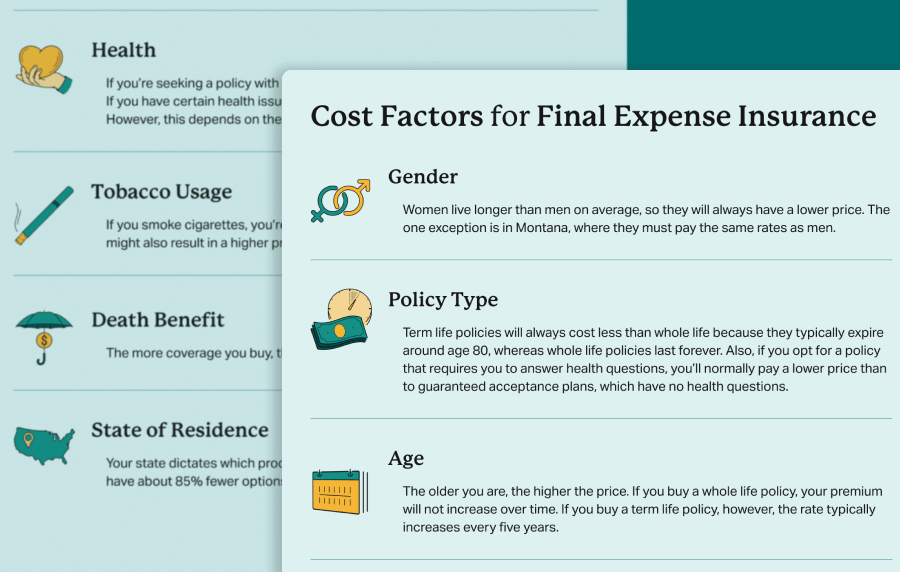

How Your Health Will Impact Your Eligibility And The Price

Some health conditions may result in higher premiums, while others may not. For example, high blood pressure (unless uncontrolled) will not result in higher premiums. On the other hand, a recent heart attack or stroke will surely result in a higher premium or be subjected to a modified plan with a two-year waiting period.

Understand that every life insurance company will have different underwriting and prices. So, while one company might charge diabetic applicants a higher premium, another might not.

As a general rule, most common issues like high cholesterol, hypertension, hyperthyroidism, arthritis, depression, anxiety, and diabetes are all easily insurable.

It’s crucial to work with a broker like Choice Mutual that can compare 10+ providers to identify which will give you the best deal based on your health and lifestyle.

Frequently Asked Questions

Whole life is not better than term life, and term life is not better than whole life. The point of life insurance is to solve a financial issue that arises specifically from your death. The specific problem you’re trying to solve is the key factor that determines which policy type is best. As a rule, only buy term insurance to cover a temporary problem, such as replacing your income or paying off a mortgage. Buy a whole life policy to cover a permanent problem, such as paying for your funeral costs.

Whole life insurance builds cash value, which is similar to a behind-the-scenes savings account. With each payment, a very small portion is directed to the cash value account, and it typically earns interest. As the cash value grows, you can withdraw it and spend it however you desire. If you ever cancel a whole life policy, the insurer will refund you however much cash value there is at the time you cancel.

Most final expense insurance companies offer a maximum coverage of $25,000-$50,000. However, some providers, such as TruStage, do offer up to $100,000 in whole life final expense coverage.

- Nationally licensed life insurance agent with over 16 years of experience.

- Personal annual production that puts him in the top .001% out of all life insurance agents in the nation.

Anthony Martin is a nationally licensed insurance expert with over 16 years of experience and has personally served over 10,000 clients with their life insurance needs. He frequently authors entrepreneurial and life insurance content for Forbes, Inc.com, Newsweek, Kiplinger, and Entreprenuer.com. Anthony has been consulted as an expert life insurance source for dozens of high-profile websites such as Forbes, Bankrate, Reuters, Fox Business, CNBC, Investopedia, Insurance.com, Yahoo Finance, and many more.

- Nationally licensed life insurance agent with over 20 years of experience

- Best selling Amazon author.

Jeff Root is a nationally licensed life insurance expert with over 20 years of experience. He has personally helped over 3000 clients with their life insurance needs. Jeff is a best-selling Amazon author and the managing partner of a highly successful insurance brokerage that manages over 2,500 licensed insurance agents across the USA. He has been a featured life insurance source for prestigious websites such as Forbes, Bloomberg, MarketWatch, Nerdwallet, and many more.

- Nationally licensed life insurance agent with over 15 years of experience

- Best selling Amazon author of five insurance sales books.

David Duford is a nationally licensed insurance expert with over 15 years of experience. He has personally helped more than 1,500 clients buy life insurance. David has been featured as an expert source for highly authoritative publications such as A.M. Best and Insurancenewsnet. He also runs one of the largest YouTube channels to help aspiring insurance agents serve their clients better.

- Nationally licensed life insurance agent with over 20 years of experience

- Best selling Amazon author.

Jeff Root is a nationally licensed life insurance expert with over 20 years of experience. He has personally helped over 3000 clients with their life insurance needs. Jeff is a best-selling Amazon author and the managing partner of a highly successful insurance brokerage that manages over 2,500 licensed insurance agents across the USA. He has been a featured life insurance source for prestigious websites such as Forbes, Bloomberg, MarketWatch, Nerdwallet, and many more.

- Nationally licensed life insurance agent with over 15 years of experience

- Best selling Amazon author of five insurance sales books.

David Duford is a nationally licensed insurance expert with over 15 years of experience. He has personally helped more than 1,500 clients buy life insurance. David has been featured as an expert source for highly authoritative publications such as A.M. Best and Insurancenewsnet. He also runs one of the largest YouTube channels to help aspiring insurance agents serve their clients better.