How Does Final Expense Insurance Work & What Does It Cover?

Final expense insurance, often called burial insurance or funeral insurance, is a special type of whole life insurance designed to cover all your end-of-life costs. It can pay for your casket, burial plot, funeral services, viewing fees, transportation, headstone/other monuments, debts, and medical bills.

When you die, the policy will pay out a tax-free cash benefit directly to your loved ones. Should they not use all the money for your final bills, they get to keep what’s left over.

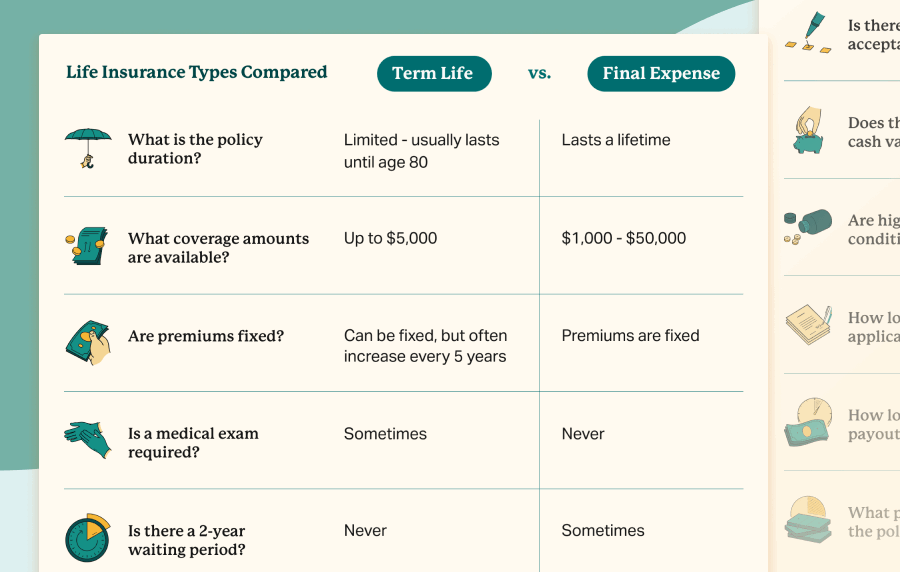

As a type of whole life insurance, there’s a contractual guarantee that coverage will never decrease, premiums will not increase, and it lasts your entire life. In addition, the policy will build cash value.

The Two Types Of Burial Insurance

There are two types of burial insurance: simplified issue and guaranteed acceptance. Both have pros and cons, so consider all angles of each option before making any decisions.

| Simplified Issue | Guaranteed Acceptance |

|---|---|

| No medical exam | No medical exam |

| Has health questions | No health questions |

| Lower premiums typically $50-100 monthly | Higher premiums typically $100+ monthly |

| Maximum coverage can be up to $100,000 | Maximum coverage usually capped at $25,000 |

| No waiting period or partial coverage | Has a 2-year waiting period |

| Approvals within 15 mins to a few days | Instant approval |

Immediate Coverage Vs Plans With A Two-Year Waiting Period

Some burial life insurance policies have a two-year waiting period, and some don’t.

To obtain an immediate benefit burial policy (aka “first day coverage”), you must apply for a plan that asks questions about your health history. No medical exam is required, but health questions are.

Understand that all guaranteed acceptance policies with no health questions have a mandatory two-year waiting period. The insurer will only refund your premiums if you die during the waiting period.

With an immediate benefit, you’re fully covered for natural or accidental death on the day your first payment is scheduled to be processed. So even if you died one day later, the insurance company would have to pay the full death benefit.

One of the most unique features of final expense insurance is that most people, even with pre-existing conditions, can qualify for day-one coverage.

How Much Does Final Expense Insurance Cost?

While the average cost of final expense insurance is $50-$100 monthly, your exact rate will depend upon age, health, gender, state of residence, tobacco usage (if any), and the death benefit you choose.

Which Insurance Companies Offer Burial Insurance?

How Do You Apply For Final Expense Life Insurance?

The requirements to apply for final expense insurance are straightforward. You must provide personal information, including name, DOB, address, SSN, phone number, beneficiaries, and payment information.

If you’re applying for a policy with no waiting period, you must also complete a health questionnaire and provide a list of your current medications. However, if you’re applying for a guaranteed issue policy, you don’t need to answer any health questions.

Ultimately, you’ll buy the policy directly from the insurer or an agency. Understanding the differences is essential because one option is far superior to the other.

- Buy directly from the insurance company: You can often sign up by mail, on their website, or by phone. If approved, they’ll mail you the policy. You’d have no specific agent assigned to your policy to contact for ongoing service issues. It’s important to note that nearly all final expense insurance companies do not sell their policies directly to consumers. Furthermore, for providers that sell directly to customers, the policies typically offer guaranteed acceptance and are more expensive, with a two-year waiting period.

- Through a broker (agency): You’ll connect with an agent in person or over the phone. They’ll generally ask you some background questions to determine which insurance provider will offer you the best burial insurance policy. If approved, the insurer will mail the policy directly to you. The most significant advantage to working with an independent agent is that they have the freedom to compare multiple insurers side by side to isolate your best option. Working with an agent has no added fees, and the insurance does not cost more. Finally, nearly all final expense companies sell their products through licensed agents. If you’re saying you won’t speak with an agent, you’re limiting yourself to about 10% of the market.

If you’re trying to buy burial insurance for a parent or grandparent, that’s acceptable, but they must participate in the application process. They’ll have to answer the health questions (if there are any) and sign the application. That’s true even if you have power of attorney over them.

How Do You File A Claim?

Filing a claim for a final expense policy is no different than any other type of life insurance. The beneficiary simply needs to call the insurance company to notify them of the death. They will send the beneficiary (by mail, fax, or email) a statement to sign and return, along with a copy of the death certificate.

These documents will allow them to process the claim and pay the prescribed death benefit.

Where burial policies differ significantly from traditional life insurance policy claims is the payout time. Final expense insurance policies typically pay out within 1-2 days after the claim is approved. Traditional life insurance plans can often take weeks or months to pay out.

Frequently Asked Questions

A final expense life insurance policy is a special type of life insurance usually meant to pay for your end-of-life costs (the payout money can technically be used for anything). A pre-paid funeral is an agreement directly with a local funeral home. You fully design your funeral and set up a payment plan to pay it off in one lump sum or via installments over time. When you die, the funeral home will execute your funeral according to your wishes.

If you can afford a pre-paid funeral (which few seniors can), it’s more useful than a final expense policy. That’s because both the funeral planning and cost components are taken care of. A final expense policy only addresses the funeral payment- not the planning. It’s worth noting that a final expense policy can be used to pay other expenses, such as medical bills or financial debts, whereas a pre-paid funeral cannot. In that respect, final expense insurance is superior.

The primary drawbacks of final expense insurance are:

- Small coverage amounts.

- Higher premiums per thousand of coverage.

- May have a two-year waiting period.

Burial insurance is a type of life insurance. That said, burial policies are very different than traditional policies. The main differences are that they offer small coverage options, the payout is super fast (typically 1-2 days), and people with high-risk medical conditions can obtain a new policy. Ultimately, though, it’s all life insurance, which means the result after you die is a cash payment to your beneficiaries.

No company sells a guaranteed issue life insurance policy with no waiting period. If there are no health questions, there will be a 2-3 year waiting period.

One of the many benefits of a whole life funeral insurance policy is that it has a fixed rate for the duration of the policy. At no point can the price increase. On the contrary, many term policies, such as those sold by Globe Life or AARP, do have a price increase every five years. So long as the policy is whole life, the premium cannot change.

Whole life burial insurance has no age limit. It will last indefinitely. As long as you faithfully make your premium payments, you’ll always be insured even if you live to be 100 years old.

The maximum age limit to buy a new policy is 90. Remember that variables such as your state of residence and health may result in a lower age cap. For example, if you live in New York, no provider sells insurance to seniors over 85.

Whole life final expense policies do accrue cash value over time. There is generally no accumulation (with any company) during the first couple of years. As the cash value builds, you can withdraw and spend it as you wish. Also, if you ever surrender the policy, the cash value will be refunded to the policy owner.

- Nationally licensed life insurance agent with over 16 years of experience.

- Personal annual production that puts him in the top .001% out of all life insurance agents in the nation.

Anthony Martin is a nationally licensed insurance expert with over 16 years of experience and has personally served over 10,000 clients with their life insurance needs. He frequently authors entrepreneurial and life insurance content for Forbes, Inc.com, Newsweek, Kiplinger, and Entreprenuer.com. Anthony has been consulted as an expert life insurance source for dozens of high-profile websites such as Forbes, Bankrate, Reuters, Fox Business, CNBC, Investopedia, Insurance.com, Yahoo Finance, and many more.

- Nationally licensed life insurance agent with over 20 years of experience

- Best selling Amazon author.

Jeff Root is a nationally licensed life insurance expert with over 20 years of experience. He has personally helped over 3000 clients with their life insurance needs. Jeff is a best-selling Amazon author and the managing partner of a highly successful insurance brokerage that manages over 2,500 licensed insurance agents across the USA. He has been a featured life insurance source for prestigious websites such as Forbes, Bloomberg, MarketWatch, Nerdwallet, and many more.

- Nationally licensed life insurance agent with over 15 years of experience

- Best selling Amazon author of five insurance sales books.

David Duford is a nationally licensed insurance expert with over 15 years of experience. He has personally helped more than 1,500 clients buy life insurance. David has been featured as an expert source for highly authoritative publications such as A.M. Best and Insurancenewsnet. He also runs one of the largest YouTube channels to help aspiring insurance agents serve their clients better.

- Nationally licensed life insurance agent with over 20 years of experience

- Best selling Amazon author.

Jeff Root is a nationally licensed life insurance expert with over 20 years of experience. He has personally helped over 3000 clients with their life insurance needs. Jeff is a best-selling Amazon author and the managing partner of a highly successful insurance brokerage that manages over 2,500 licensed insurance agents across the USA. He has been a featured life insurance source for prestigious websites such as Forbes, Bloomberg, MarketWatch, Nerdwallet, and many more.

- Nationally licensed life insurance agent with over 15 years of experience

- Best selling Amazon author of five insurance sales books.

David Duford is a nationally licensed insurance expert with over 15 years of experience. He has personally helped more than 1,500 clients buy life insurance. David has been featured as an expert source for highly authoritative publications such as A.M. Best and Insurancenewsnet. He also runs one of the largest YouTube channels to help aspiring insurance agents serve their clients better.