Original Research

We publish regular studies and conduct surveys to provide you with accurate, reliable, and up-to-date information on insurance topics, senior issues, and end-of-life matters.

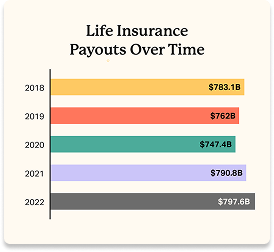

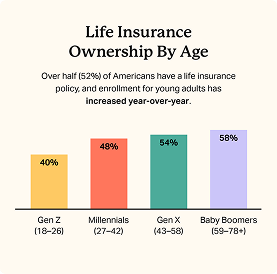

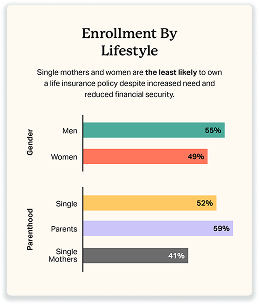

Life Insurance Statistics, Facts, and Trends For 2026

Get the most current life insurance statistics on the benefits of coverage, evolving consumer beliefs and trends, and the growing insurance industry.

See the trends

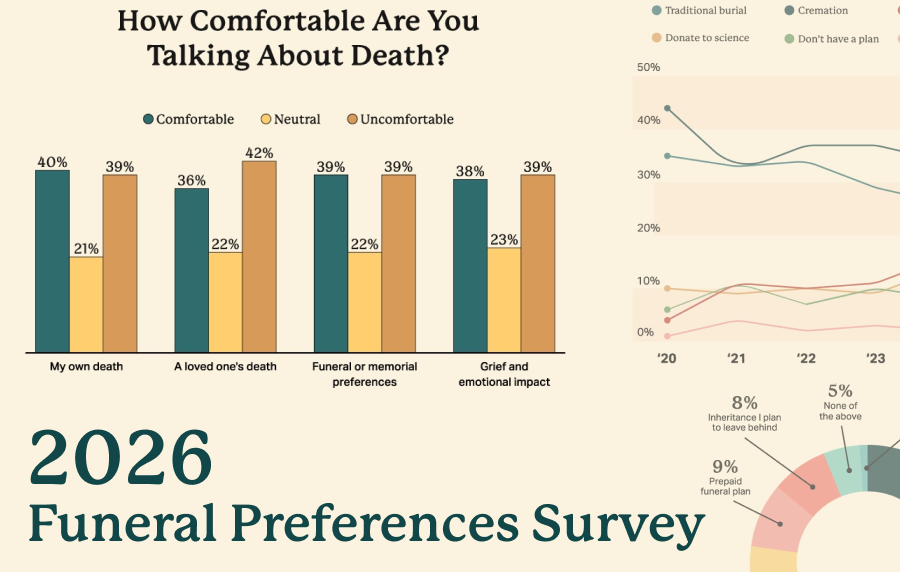

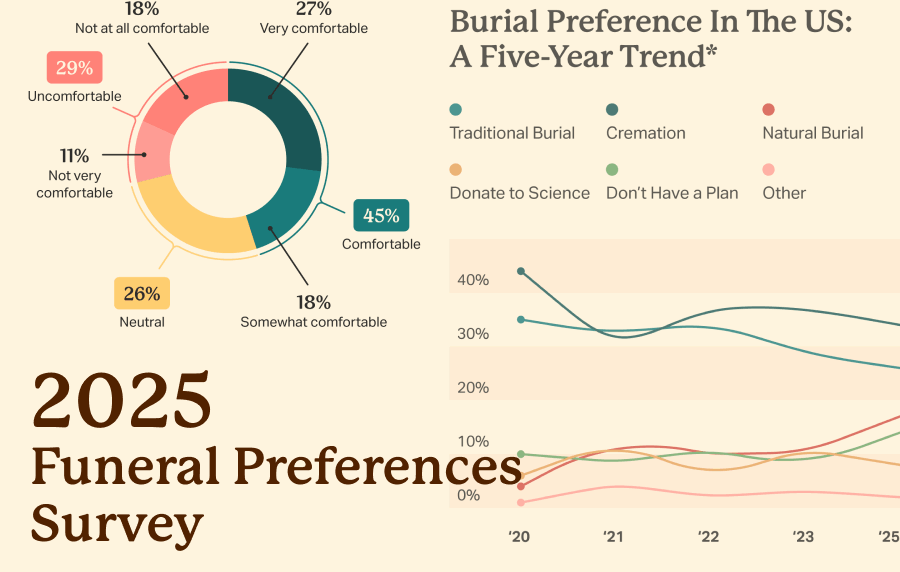

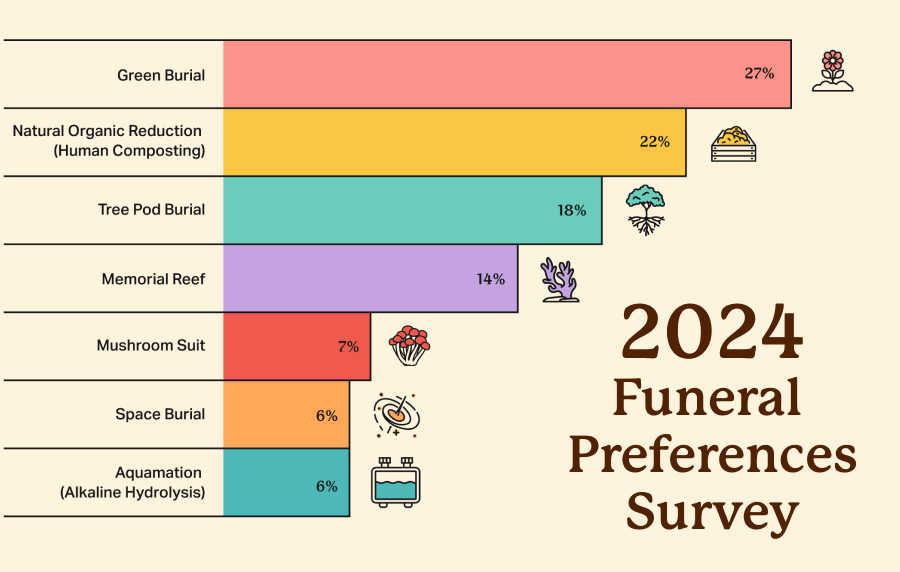

Annual Funeral Preferences Surveys

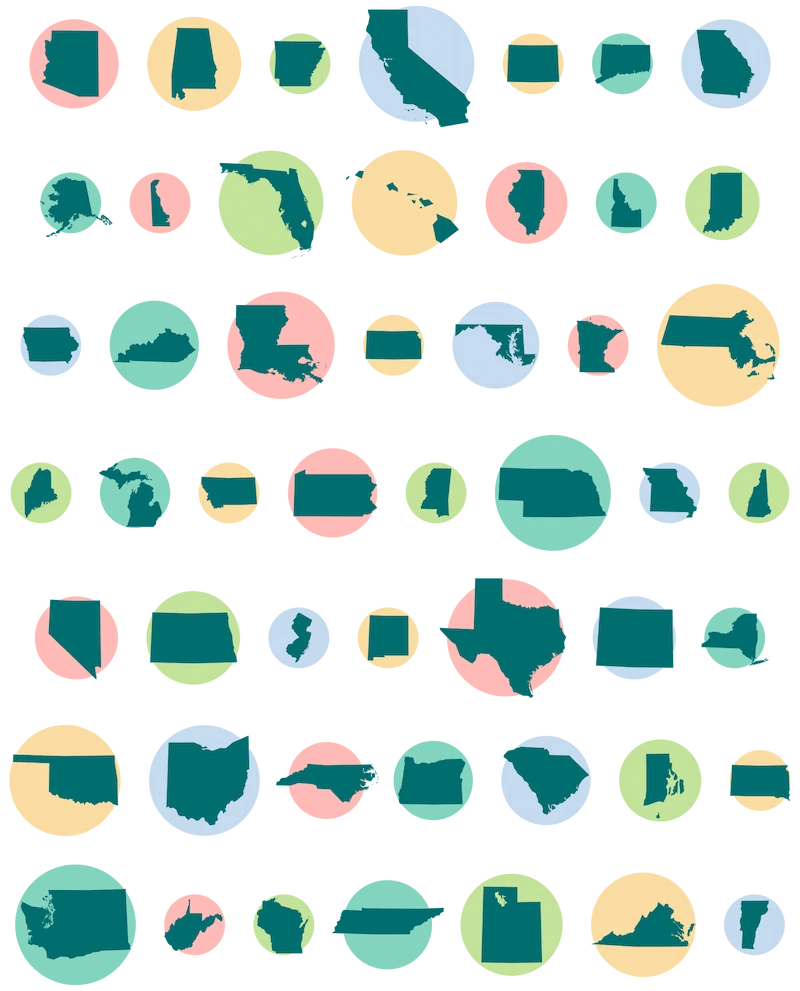

Final Resting Places Across America

Eternal Neighbors: The Famous Figures That Americans Find Most Inspiring

If given the choice, which famous person would you most like to be buried beside? Our survey of over 3,000 people offers a unique angle on American values and interests.

Explore the survey