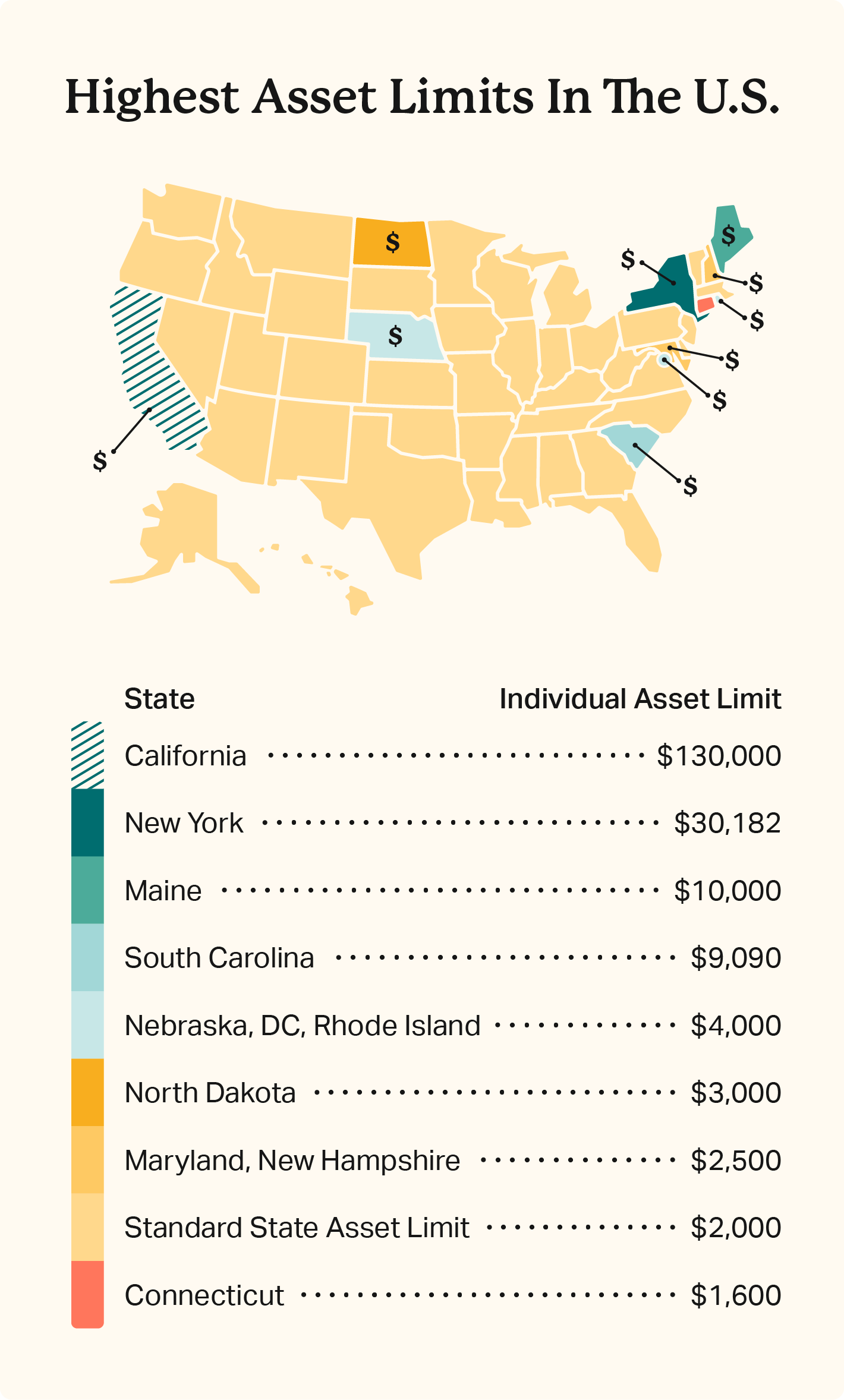

Asset Limits For Medicaid

Asset limits are the dollar values of countable assets, such as bank accounts, stocks, and bonds. Seniors and people with disabilities enrolled in regular Medicaid typically have an asset limit of $2,000 for individuals and $3,000 for couples, though this varies by state.

Resource limits for disabled Medicaid recipients who work or receive long-term care, nursing support, or institutionalized care may vary.

It’s not as common, but some states enforce asset limits for other eligibility groups. This is particularly true for medically needy individuals and parents/caretakers receiving Medicaid assistance.

Meanwhile, several states have updated their limits in 2026. California reinstated asset limits for Non-MAGI Medi-Cal applicants, setting $130,000 for individuals and $195,000 for couples. At the same time, Maine increased exemptions, effectively raising the limits to $ 10,000 and $15,000 for singles and couples, respectively.

| State | Individual Asset Limit | Couple Asset Limit |

|---|---|---|

| Alabama | $2,000 | $3,000 |

| Alaska | $2,000 | $3,000 |

| Arizona | $2,000 | $3,000 |

| Arkansas | $2,000 | $3,000 |

| California | $130,000 | $195,000 |

| Colorado | $2,000 | $3,000 |

| Connecticut | $1,600 | $2,400 |

| Delaware | $2,000 | $3,000 |

| District of Columbia | $4,000 | $6,000 |

| Florida | $2,000 | $3,000 |

| Georgia | $2,000 | $4,000 |

| Hawaii | $2,000 | $3,000 |

| Idaho | $2,000 | $3,000 |

| Illinois | $2,000 | $3,000 |

| Indiana | $2,000 | $3,000 |

| Iowa | $2,000 | $3,000 |

| Kansas | $2,000 | $3,000 |

| Kentucky | $2,000 | $4,000 |

| Louisiana | $2,000 | $3,000 |

| Maine | $10,000 | $15,000 |

| Maryland | $2,500 | $3,000 |

| Massachusetts | $2,000 | $3,000 |

| Michigan | $2,000 | $3,000 |

| Minnesota | $3,000 | $6,000 |

| Mississippi | $2,000 | $3,000 |

| Missouri | $2,000 | $3,000 |

| Montana | $2,000 | $3,000 |

| Nebraska | $4,000 | $6,000 |

| Nevada | $2,000 | $3,000 |

| New Hampshire | $2,500 | $4,000 |

| New Jersey | $2,000 | $3,000 |

| New Mexico | $2,000 | $3,000 |

| New York | $30,182 | $40,821 |

| North Carolina | $2,000 | $3,000 |

| North Dakota | $3,000 | $6,000 |

| Ohio | $2,000 | $3,000 |

| Oklahoma | $2,000 | $3,000 |

| Oregon | $2,000 | $3,000 |

| Pennsylvania | $2,000 | $3,000 |

| Rhode Island | $4,000 | $6,000 |

| South Carolina | $9,090 | $13,630 |

| South Dakota | $2,000 | $3,000 |

| Tennessee | $2,000 | $3,000 |

| Texas | $2,000 | $3,000 |

| Utah | $2,000 | $3,000 |

| Vermont | $2,000 | $3,000 |

| Virginia | $2,000 | $3,000 |

| Washington | $2,000 | $3,000 |

| West Virginia | $2,000 | $3,000 |

| Wisconsin | $2,000 | $3,000 |

| Wyoming | $2,000 | $3,000 |

Countable vs. Exempt Assets For Medicaid

Countable assets are typically your liquid resources — bank balances, certificates of deposit, stocks, bonds, and more. Cash and cash equivalents are considered part of your Medicaid asset limit.

The value of exempt assets doesn’t count toward asset limits. This includes personal property and lifestyle assets, such as:

- Primary residence

- Personal vehicle

- Burial insurance

- Preplanned funeral agreements

- Jewelry

- Decor

- Clothes

Here’s an example of how your assets might be counted:

| Asset Type | Value |

|---|---|

| Total assets | $50,000 |

| Exempt assets | $20,000 |

| Countable assets for Medicaid | $30,000 |

State guidelines differ, with some allowing more exemptions than others when determining which assets are countable vs. exempt.

Rules on how your spouse’s personal property and assets count toward an asset limit also vary. Couples have higher asset limits, as all countable assets owned by either party are considered for Medicaid eligibility. However, asset limits remain quite low and don’t provide families much flexibility for savings and emergencies.

Federal and state spousal impoverishment programs are available to support the partners of Medicaid recipients. These allow additional resources for partners of Medicaid recipients receiving long-term or institutional care, such as assisted living.

Medicaid Eligibility

Asset limits are a minor factor in Medicaid eligibility, primarily affecting Aid to the Aged, Blind, or Disabled (AABD).

Eligibility depends on multiple factors, including health metrics, and varies by state. The table below summarizes the main eligibility factors and the groups that may qualify for Medicaid:

| Asset Type | Value |

|---|---|

| Eligibility Factors | Income, health condition, age, and asset limits |

| Primary Groups Affected by Asset Limits | Seniors / Aged, Blind, Disabled (AABD) |

| Other Eligible Groups | Children, pregnant women, parents/caretakers, low-income adults (19–64) |

Federal Medicaid guidelines require coverage for select groups, including children, pregnant people, and the Aged, Blind, and Disabled (ABD).

Low-income adults without a disability aged 19-64 may also qualify for coverage under Medicaid Expansion. So far, 41 U.S. states have adopted expanded coverage, excluding:

- Alabama

- Florida

- Georgia

- Kansas

- Mississippi

- South Carolina

- Tennessee

- Texas

- Wisconsin

- Wyoming

What To Do If You Exceed Medicaid Financial Eligibility Limits

Medicaid resource limits are tight, and additional assets like an end-of-year bonus or raise at work can affect your eligibility. If you have too many countable assets to qualify, you have a few options.

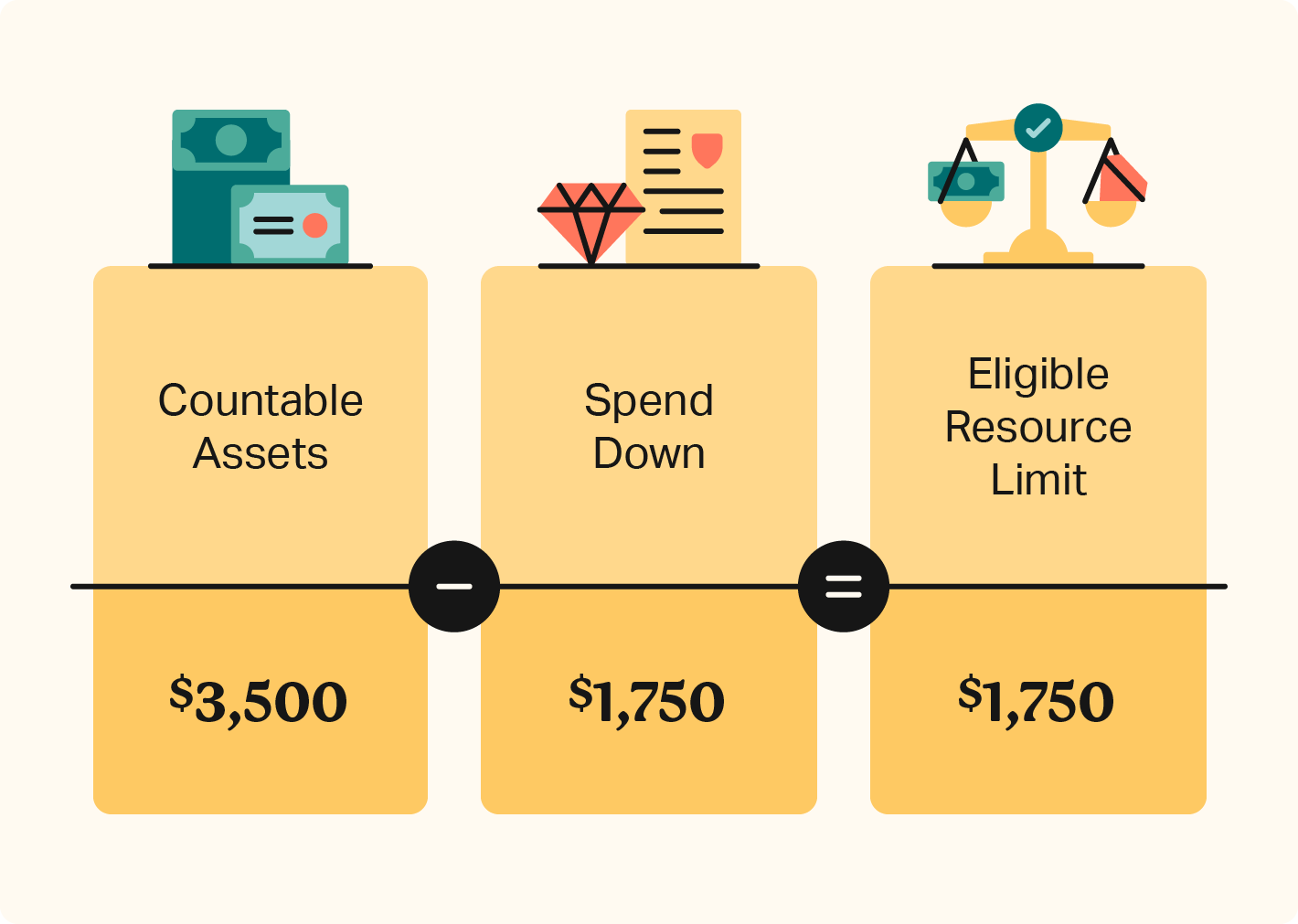

Medicaid spend down

Spend down involves using or reallocating your liquid assets to reduce your countable resources and meet eligibility requirements.

You can spend your money outright on debt or physical items like jewelry. Debt repayment is ideal, as it reduces liabilities and may lower monthly payments. However, something like jewelry or art can still contribute to your wealth without impacting your health care.

Alternatively, you can purchase exempt services, such as final expense insurance. This allocates funds to your future end-of-life care and estate, ensuring your final expenses are covered while reducing your current liquid assets.

Be aware that Medicaid has a look-back period that evaluates all asset transfers you and your spouse made over five years before the Medicaid application. Penalties may apply to any gifted transfers of assets sold below market value.

Alternative state assistance

States, counties, and municipalities often manage additional social services that may support your financial and medical needs. Contact your local health and human services department to explore non-Medicaid support options provided by government and nonprofit agencies.

Provided services may include:

- SNAP food stamps and nutritional assistance

- Child care assistance

- TANF temporary financial assistance

- Home energy assistance

- Housing and shelter assistance

How To Apply For Medicaid

You can apply for Medicaid assistance through the federal Health Insurance Marketplace regardless of your state of residence. State Medicaid agencies also assist applicants.

Most states accept online and paper applications submitted in person or by mail. Phone assistance is also available. Contact your state’s Medicaid or Health and Human Services office to learn more.

Protect Your Coverage And End-Of-Life Plan

Carefully managing your assets helps you stay within Medicaid limits while preparing for future expenses. Allocating funds toward exempt assets or planning for final expenses can reduce countable assets without leaving gaps in your financial plan.

Life insurance is one way to plan ahead, helping cover funeral or burial costs while reducing countable assets. Choice Mutual provides guidance to help you understand how these options fit alongside your overall plan and state requirements.

If you’re interested in exploring your options, get a personalized quote to see what may work for your situation.

- Nationally licensed life insurance agent with over 16 years of experience.

- Personal annual production that puts him in the top .001% out of all life insurance agents in the nation.

Anthony Martin is a nationally licensed insurance expert with over 16 years of experience and has personally served over 10,000 clients with their life insurance needs. He frequently authors entrepreneurial and life insurance content for Forbes, Inc.com, Newsweek, Kiplinger, and Entreprenuer.com. Anthony has been consulted as an expert life insurance source for dozens of high-profile websites such as Forbes, Bankrate, Reuters, Fox Business, CNBC, Investopedia, Insurance.com, Yahoo Finance, and many more.

- Nationally licensed life insurance agent with over 20 years of experience

- Best selling Amazon author.

Jeff Root is a nationally licensed life insurance expert with over 20 years of experience. He has personally helped over 3000 clients with their life insurance needs. Jeff is a best-selling Amazon author and the managing partner of a highly successful insurance brokerage that manages over 2,500 licensed insurance agents across the USA. He has been a featured life insurance source for prestigious websites such as Forbes, Bloomberg, MarketWatch, Nerdwallet, and many more.

- Nationally licensed life insurance agent with over 15 years of experience

- Best selling Amazon author of five insurance sales books.

David Duford is a nationally licensed insurance expert with over 15 years of experience. He has personally helped more than 1,500 clients buy life insurance. David has been featured as an expert source for highly authoritative publications such as A.M. Best and Insurancenewsnet. He also runs one of the largest YouTube channels to help aspiring insurance agents serve their clients better.

- Nationally licensed life insurance agent with over 20 years of experience

- Best selling Amazon author.

Jeff Root is a nationally licensed life insurance expert with over 20 years of experience. He has personally helped over 3000 clients with their life insurance needs. Jeff is a best-selling Amazon author and the managing partner of a highly successful insurance brokerage that manages over 2,500 licensed insurance agents across the USA. He has been a featured life insurance source for prestigious websites such as Forbes, Bloomberg, MarketWatch, Nerdwallet, and many more.

- Nationally licensed life insurance agent with over 15 years of experience

- Best selling Amazon author of five insurance sales books.

David Duford is a nationally licensed insurance expert with over 15 years of experience. He has personally helped more than 1,500 clients buy life insurance. David has been featured as an expert source for highly authoritative publications such as A.M. Best and Insurancenewsnet. He also runs one of the largest YouTube channels to help aspiring insurance agents serve their clients better.

Choice Mutual often cites third-party websites to provide context and verification for specific claims made in our work. We only link to authoritative websites that provide accurate information. You can learn more about our editorial standards, which guide our mission of delivering factual and impartial content.

-

spousal impoverishment programs. https://www.medicaid.gov/medicaid/eligibility/spousal-impoverishment/index.html

-

require coverage for select groups. https://www.medicaid.gov/sites/default/files/2019-12/list-of-eligibility-groups.pdf

-

SNAP. http://www.fns.usda.gov/snap/supplemental-nutrition-assistance-program-snap

-

TANF. https://www.acf.hhs.gov/ofa/map/about/help-families

-

Home energy assistance. https://www.acf.hhs.gov/ocs/low-income-home-energy-assistance-program-liheap

-

$1,600/$2,400. https://www.medicaidplanningassistance.org/medicaid-eligibility-connecticut/

-

$195,000. https://www.medicaidplanningassistance.org/medicaid-eligibility-california/