What Type Of Life Insurance Can Seniors Over 85 Get?

Final expense life insurance is the only type of policy available to seniors over 85, and 90 is the maximum age limit for new applicants.

A final expense policy is a small whole life insurance plan that doesn’t require a medical exam to qualify. “Final expense insurance” is also frequently referred to as “burial insurance” or “funeral insurance.”

For seniors above age 85, $10,000 – $25,000 is the most coverage you can buy from any provider. However, you can buy more than one policy from different companies.

Like all forms of life insurance, final expense policies pay the death benefit as a tax-free cash payment upon the insured’s death. Your loved ones can spend the money on funeral costs, medical bills, debts, or anything else (no restrictions).

Because these policies are a type of whole life insurance, they build cash value; the payments will never increase, coverage will never decrease, and they last forever.

What about burial insurance?

Some people believe that burial insurance differs from life insurance, which is false. Burial insurance is life insurance (read burial vs. life insurance).

A burial only happens when someone dies, which is why final expense insurance is a type of life insurance.

Final Expense Life Insurance Companies For Seniors Over 85

Below are the five providers that offer life insurance to seniors over 85. Remember, these funeral life insurance companies may not be available in all states.

Y2 50% payout,

Y3+ full benefits

How Much Does Burial Insurance Over Age 85 Cost?

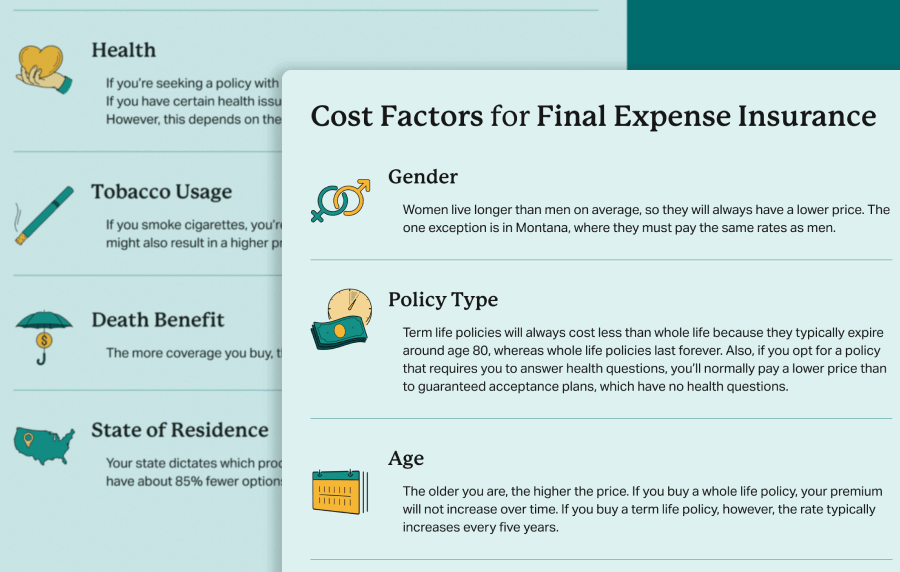

The cost of life insurance for seniors over 80 could be as low as $80 per month or as much as $800. The net price is determined by age, gender, health, state of residence, tobacco usage, and the coverage amount.

That being said, below are some sample online final expense quotes. As you can see from the sample rates below, getting final expense insurance for senior citizens at this age is costly. The only way to secure lower prices would be to buy less coverage ($2,000 is the absolute minimum).

Do Final Expense Policies Over Age 85 Have A Waiting Period?

Of the five companies that offer life insurance over 85, four of them have no waiting period. The remaining company has a partial waiting period during the first two years.

The most important thing to understand is that you must qualify for life insurance that starts immediately (at any age).

You don’t have to take a medical exam to get a no-waiting period policy, but you will have to answer health questions.

Please don’t assume you won’t qualify because you have pre-existing conditions. Despite high-risk medical issues, seniors above 85 can still qualify for an immediate plan.

It’s beneficial to speak with a licensed independent agency with access to multiple providers. They can quickly diagnose what you may or may not qualify for.

States Where Seniors Over 86+ Cannot Get Life Insurance

New York is the only state in the USA with no life insurance options for those over the age of 85.

All other states (including DC) have products available for ages 86+.

Insurance companies must select each state in which they want to offer their products, and they avoid New York because of the overly burdensome regulations that don’t exist in other states.

Is There Guaranteed Acceptance Life Insurance For Seniors Over 85?

No providers offer a no-health-question guaranteed issue policy after age 85. Guaranteed acceptance plans are only available at age 85 and below.

You’ll have to answer health questions to get life insurance between the age of 86-90.

How To Apply For Life Insurance For Elderly Seniors Over 85

First, you must verbally speak with a licensed agent. There is no way to apply via mail or entirely online.

If you’re unwilling to speak to an agent via telephone, you cannot get life insurance for a senior over 85.

That said, here’s how the process works.

- Your agent will read the health questions to the person who will be insured and gather all the necessary information to complete the application.

- You’ll sign the application either verbally or electronically via email or text.

- Once signed, the application will be submitted to underwriting. Generally, the companies will approve or decline applications within 15 minutes and 24 hours.

If your application is approved, you’ll get the physical paper policy via US mail within two to three weeks.

You don’t have to make a down payment. You can choose when the premiums begin, which is when the insurance will start.

If you need coverage for someone over 85, call us at 1-800-644-2926. We can assist you with any of the companies you see on this page.

Non-Insurance End-of-Life Planning Options

If you don’t want life insurance over 85 due to the cost or for some other reason, there are other ways to pay for a funeral outside of insurance, such as:

- Religiously put money into a savings account.

- Contact local funeral homes to see if you can start pre-paying for a funeral plan.

- Rely on your estate to pay for your final expenses. Assuming you have some valuable assets, your loved ones can sell them to pay for your funeral costs. Granted, this is a less-than-ideal game plan since it will likely take many months to process everything.

The financial aspect aside, everyone should aim to plan their own funeral. Doing so ahead of time will ensure your loved ones do not have to make those tough decisions when you pass away.

You can document your final wishes on any sheet of paper or download a free online guide.

Frequently Asked Questions

Most life insurance for those over 85 has no waiting period. Only one company offers a policy that has a partial waiting period during the first 24 months. The rest of the companies only offer an immediate benefit if you qualify.

In most cases, Aetna is the best life insurance company for seniors 86 years or older. That’s because they have the lowest rates relative to other companies at this age, and they will accept applicants with a wide variety of pre-existing conditions. Plus, Aetna has been in business since 1853 and has an A rating with AM Best, so you can trust they will have the means to pay your claim.

Many providers offer life insurance for seniors with no medical exam. However, once you’re above the age of 85, you will need to answer questions about your medical history. After 85, there are no policies with no health questions (guaranteed acceptance).

Yes, you can buy life insurance for your elderly parents. However, your parents or grandparents must participate in the application process. They must answer the health questions and agree that you are purchasing the policy on their behalf.

Life insurance for seniors over 85 is expensive because of your age. Since people over 85 don’t typically live a very long time, offering them life insurance is risky. With all forms of insurance, a higher risk translates into a higher cost.

The incontestability clause is present in every life insurance contract, regardless of which provider you buy from or the type of policy.

This provision exists in every life insurance policy.

The incontestability clause entitles the insurance company to investigate any death during the first 24 months of the policy (in some states, it’s only 12 months).

Basically, they will order copies of your medical records to ensure you didn’t misrepresent your health when you first applied.

They will deny the claim if they find evidence that you had a medical condition (before the application) that would have caused them to decline you for coverage.

However, they will pay the entire death benefit if they find you answered the questions honestly.

If they deny a claim due to health misrepresentation, they will refund 100% of the paid premiums. It’s important to remember that insurance companies can not investigate death claims after the incontestability clause expires. They must simply pay the claim.

Here are a few critical points to keep in mind about the incontestability clause:

- Life insurance with no incontestability clause does not exist.

- You have nothing to worry about if you’re honest when you apply.

- Waiting periods are different from the incontestability period. A waiting period means there is no chance of a payout in the first 24 months.

- Health issues you develop after the policy is issued are not pertinent. Only medical conditions before applying are relevant when investigating a contestable claim.

Just answer the health questions honestly, and you can feel comfortable knowing that your claim will be paid even if you die the next day.

- Nationally licensed life insurance agent with over 16 years of experience

- Personal annual production that puts him in the top .001% out of all life insurance agents in the nation.

Anthony Martin is a nationally licensed insurance expert with over 16 years of experience and has personally served over 10,000 clients with their life insurance needs. He frequently authors entrepreneurial and life insurance content for Forbes, Inc.com, Newsweek, Kiplinger, and Entreprenuer.com. Anthony has been consulted as an expert life insurance source for dozens of high-profile websites such as Forbes, Bankrate, Reuters, Fox Business, CNBC, Investopedia, Insurance.com, Yahoo Finance, and many more.

- Nationally licensed life insurance agent with over 20 years of experience

- Best selling Amazon author.

Jeff Root is a nationally licensed life insurance expert with over 20 years of experience. He has personally helped over 3000 clients with their life insurance needs. Jeff is a best-selling Amazon author and the managing partner of a highly successful insurance brokerage that manages over 2,500 licensed insurance agents across the USA. He has been a featured life insurance source for prestigious websites such as Forbes, Bloomberg, MarketWatch, Nerdwallet, and many more.

- Nationally licensed life insurance agent with over 15 years of experience

- Best selling Amazon author of five insurance sales books.

David Duford is a nationally licensed insurance expert with over 15 years of experience. He has personally helped more than 15,000 clients buy life insurance. David has been featured as an expert source for highly authoritative publications such as A.M. Best and Insurancenewsnet. He also runs one of the largest Youtube channels to help aspiring insurance agents serve their clients better.

- Nationally licensed life insurance agent with over 20 years of experience

- Best selling Amazon author.

Jeff Root is a nationally licensed life insurance expert with over 20 years of experience. He has personally helped over 3000 clients with their life insurance needs. Jeff is a best-selling Amazon author and the managing partner of a highly successful insurance brokerage that manages over 2,500 licensed insurance agents across the USA. He has been a featured life insurance source for prestigious websites such as Forbes, Bloomberg, MarketWatch, Nerdwallet, and many more.

- Nationally licensed life insurance agent with over 15 years of experience

- Best selling Amazon author of five insurance sales books.

David Duford is a nationally licensed insurance expert with over 15 years of experience. He has personally helped more than 15,000 clients buy life insurance. David has been featured as an expert source for highly authoritative publications such as A.M. Best and Insurancenewsnet. He also runs one of the largest Youtube channels to help aspiring insurance agents serve their clients better.

Choice Mutual often cites third-party websites to provide context and verification for specific claims made in our work. We only link to authoritative websites that provide accurate information. You can learn more about our editorial standards, which guide our mission of delivering factual and impartial content.

-

incontestability clause. https://www.investopedia.com/terms/i/incontestability-clause.asp

-

download a free online guide. http://mdcps.fbmcbenefitscommunications.com/assets/30517---full-funeral-guide.pdf

-

Get Quotes. https://securitynationallife.com/for-individuals-families/final-expense-insurance/

-

AM Best. https://news.ambest.com/pr/PressContent.aspx?altsrc=2&refnum=34492